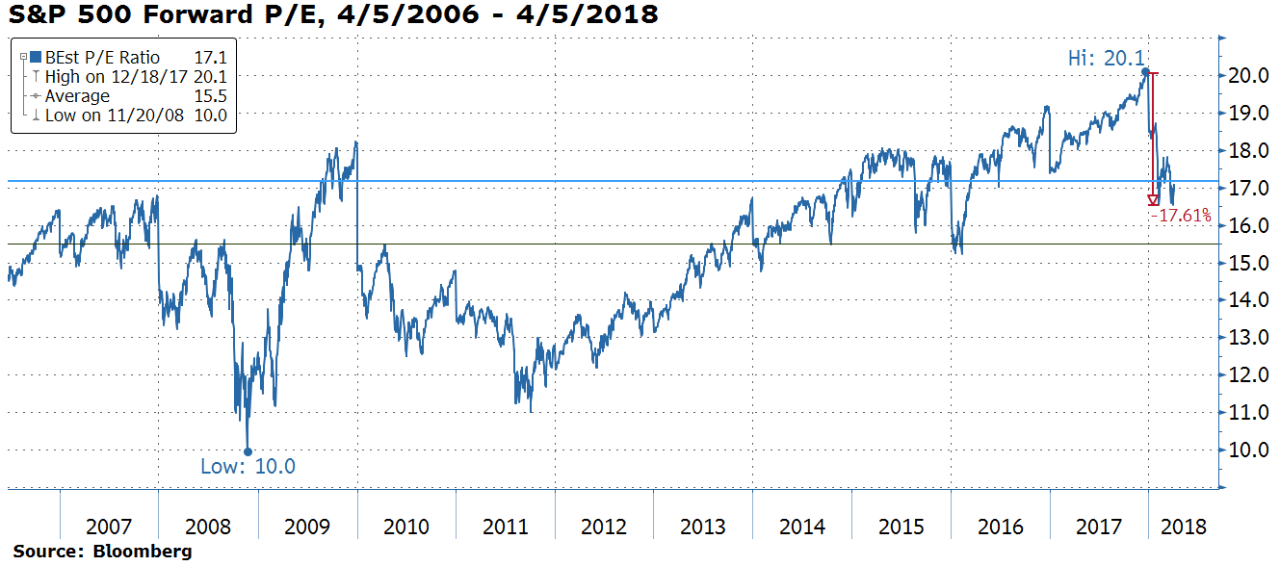

Valuations remain elevated for US stocks. For instance, the S&P 500’s forward P/E rose above 20 going into 2018. Since then volatile and declining stock prices have pushed the ratio down to below 17.

The chart below shows the S&P 500 Forward P/E Ratio since April of 2006:

Click to enlarge

Source: Focus on Fundamentals, Legg Mason