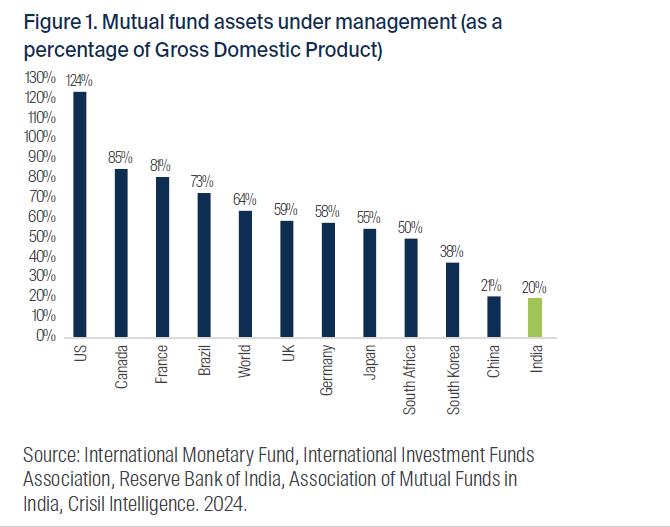

The Mutual Funds industry is one of the top industries in the US holding billions or even trillions of dollars of investors’ assets under management. As a percentage of GDP, the industry’s Assets Under Management(AUM) is the highest in the US followed by Canada and France. India has the lowest percentage at only 20% behind China.

Click to enlarge

Source: India’s Investment Boom, FSSA Investment Managers