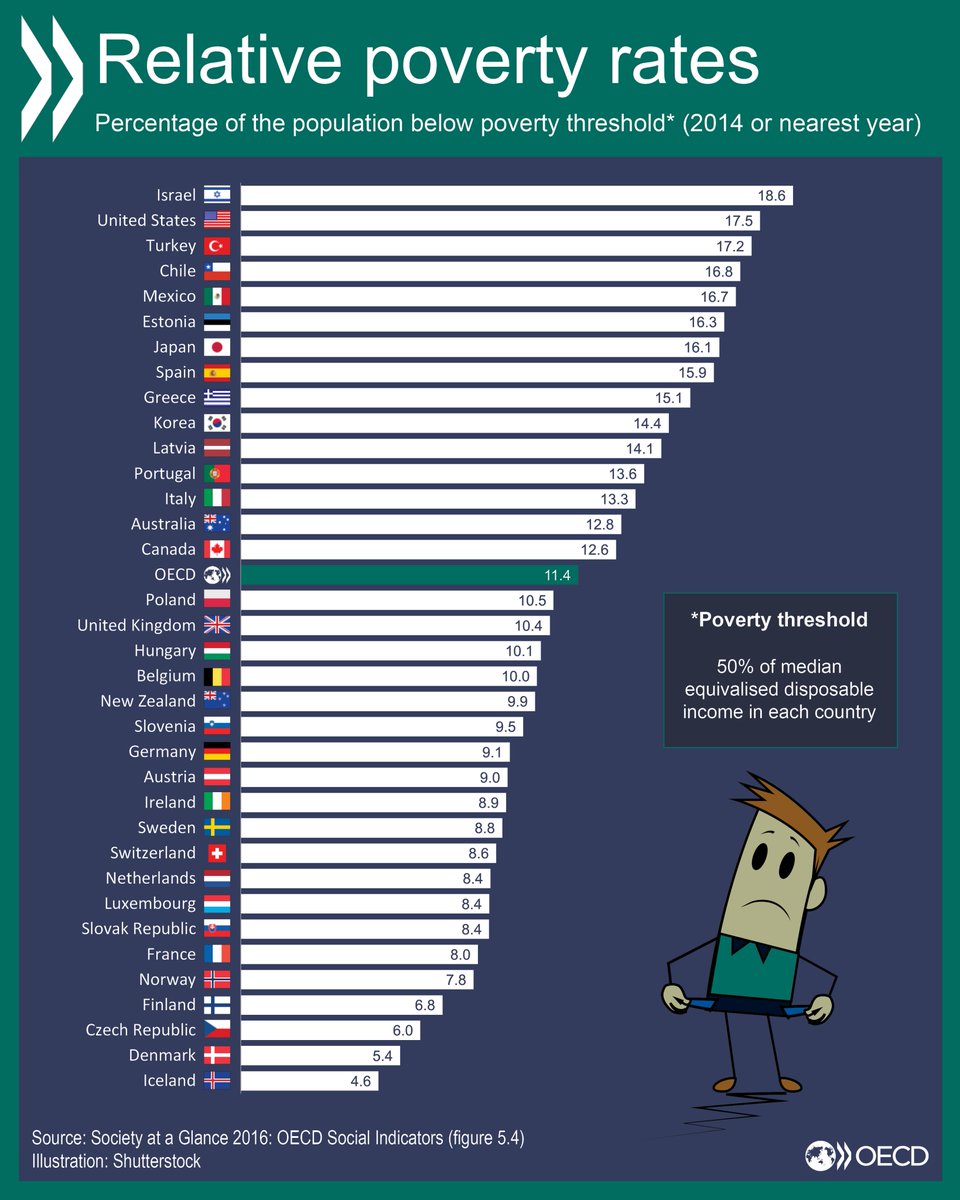

The percentage of population living below the poverty threshold levels across OECD member countries are shown in the chart below:

Click to enlarge

Source: Society at a Glance 2016, OECD

The U.S. ranks second in this list with only Israel having higher percentage.

The current poverty threshold level in the US is $24,300 for a family of four persons. Households earning above this threshold are not considered poor according to the state. Obviously this level is very low. It is not possible for couple with two children earning let’s say $30,000 per year live a comfortable life anywhere in the country. In the bigger cities and major metropolitan areas $30K won’t go far – probably may cover only the annual rental for an apartment…..