Global trade is important in the modern era. With globalization, goods are moved across borders benefiting many countries during the process.

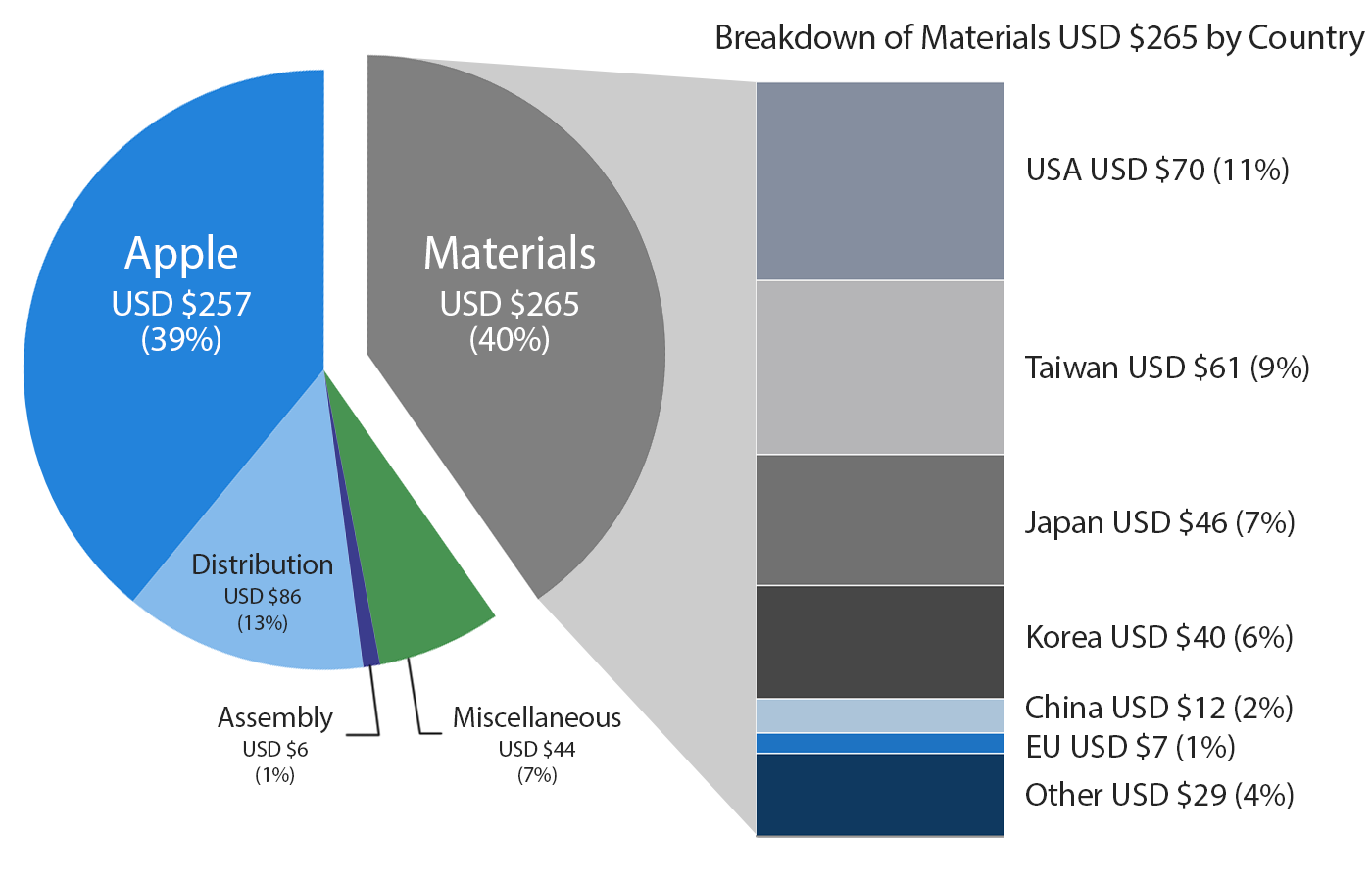

The breakdown of a popular product such as iPhone 7 shows the benefits of global trade. The phone sells for $658 in the U.S. Of this, about 40% or 257$ goes to Apple(AAPL) and other U.S. companies make $70 ( or 11%) out of it. So in total, about half of the cost of the iPhone goes to US firms.

Component makers Korea, Taiwan and Japan take 6%, 9% and 7% respectively. China, the assembler and shipper of the product gets only 2% of the retail price.

So in summary, just 2% of an iPhone’s price goes to China. Though China is blamed for the destruction of US manufacturing jobs and profiting from it, at least in the case of Apple’s iPhone the biggest gainer is US and not China.

The following chart shows the breakdown of iPhone 7 price:

Click to enlarge

Source: The Real Trade War, by ,

Also see: Breakdown of an Apple iPhone 5 Component Costs, TFS

Update:

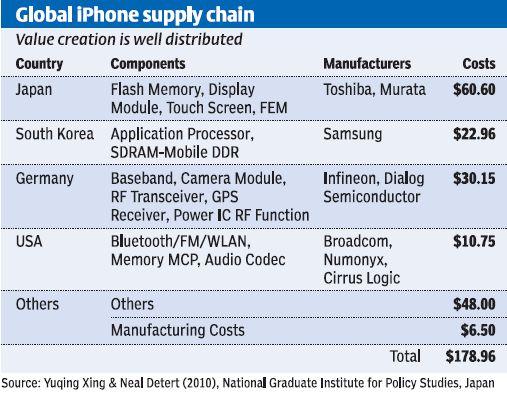

Global iPhone Supply Chain

Source: The Hindu BusinessLine

Disclosure: No Positions