Safran SA(SAFRY), the French aerospace, defense and security firm has announced a stock split in the rate of 300%. The ADR Record Date is Nov 6, 2013 and the Payable Date is Nov 7, 2013.

Currently the ADR to Ordinary ratio is 1: 1. As a result of the split, the ratio will change as 1 Ordinary to 4 ADRs. Hence ADR shareholders will receive 3 additional shares for each ADR held as of Nov 6, 2013 per a release by Citibank, the depository for this ADR program.

Here are some key facts from Safran’s Website:

SAFRAN AT A GLANCE (2012)

62,500 employees worldwide

€13,560 billion in sales

€1.6 billion in R&D expenditures

MARKET POSITIONS

No. 1 worldwide in engines for mainline commercial jets (partnership with GE)

No. 1 worldwide in landing gear, wheels and carbon brakes

No. 1 worldwide in helicopter flight controls

No. 1 worldwide in multi-biometric technology

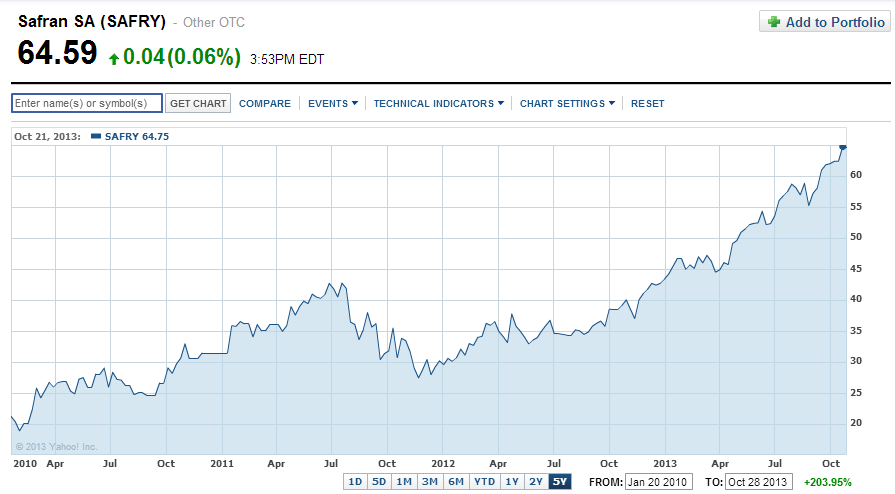

The stock has more than doubled in the past 5 years as shown in the chart below:

Click to enlarge

Source: Yahoo Finance

Currently SAFRY has a 1.96% dividend yield.

Disclosure: No Positions