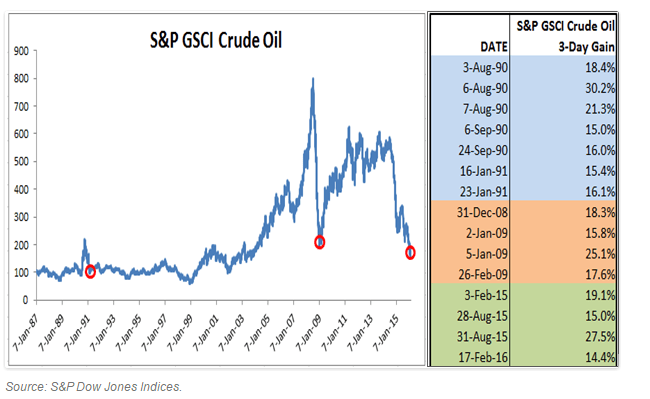

Brent oil prices closed at $34.87 yesterday. Oil prices have rebounded sharply in the past three days. According to a report by S&P, oil price gains of this magnitude have occurred only around bottoms.

Click to enlarge

Source: Oil Gains This Big Only Happen Around Bottoms, S&P Indexology