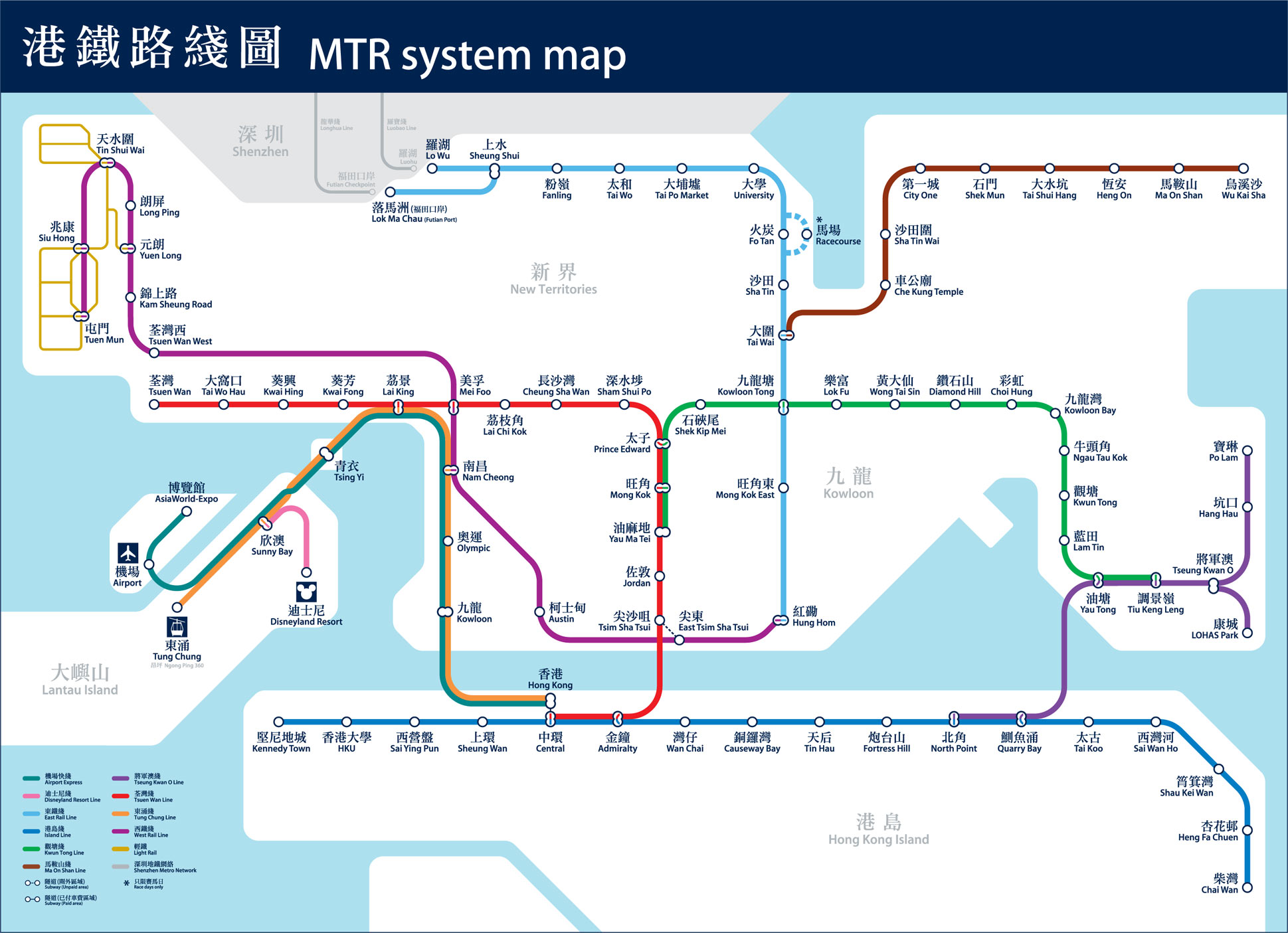

The Mass Transit Railway (MTR) of Hong Kong covers 135 miles with 155 stations. It is one of the world’s profitable transit systems. The system is operated by MTR Corporation Limited. The company’s stock trades on the OTC market under the ticker MTRJY. Currently it has a market cap of over $32.0 billion.

Click to enlarge

Source: MTR

Download: Hong Kong Metro Map (in pdf)

Earlier: Shanghai Subway Map 2016