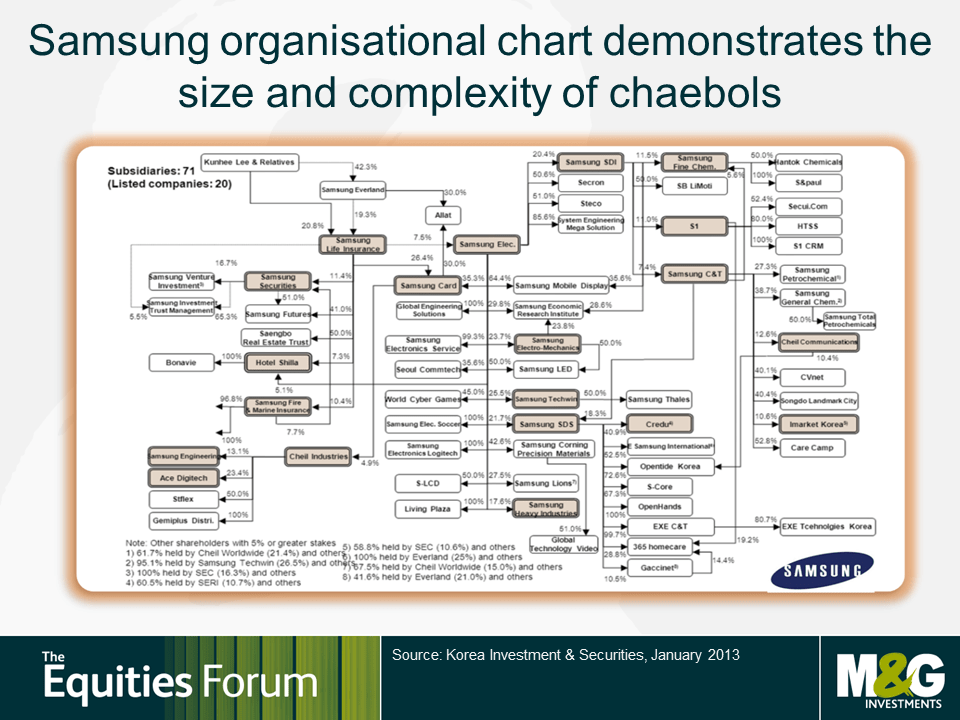

The South Korean economy is dominated by a handful of Chaebols. One of these conglomerates is Samsung. The following chart shows the size and complexity of Samsung:

Click to enlarge

Source: Why a horse named Vitana V might be good news for Korean equities, The Equities Forum, M&G Investments

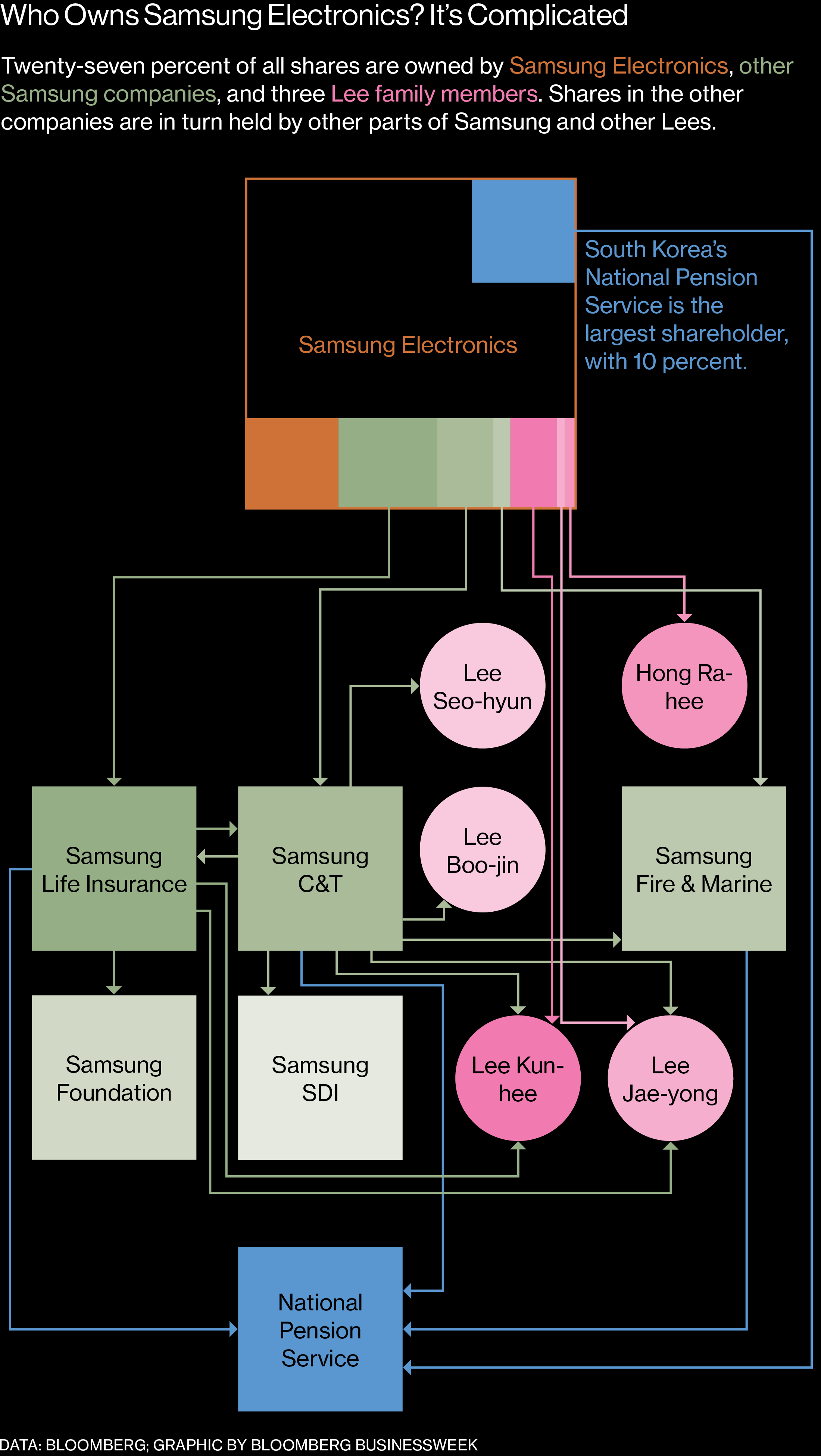

Update (Aug, 2017):

Samsung Ownership Structure-2017

Click to enlarge

Source: Summer of Samsung: A Corruption Scandal, a Political Firestorm—and a Record Profit, Bloomberg BusinessWeek

Also see: