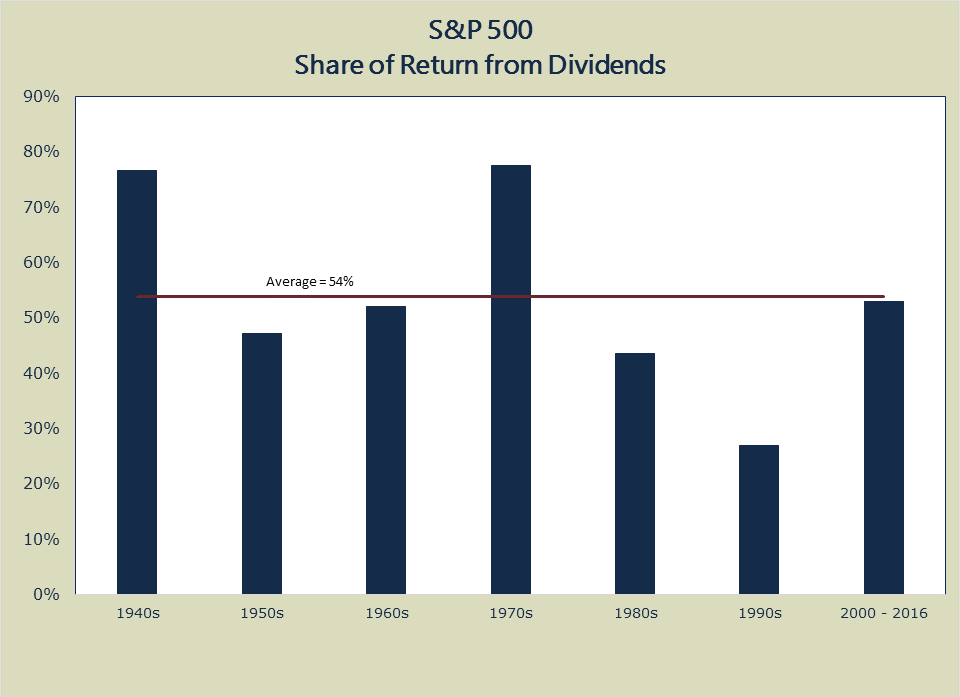

One of the new features that I have added on this site is the Dividend History of Stocks. Currently the dividend history of all the components of the Dow are posted. More dividend history pages of other companies will be added regularly.

You can check out the dividend history pages by clicking on the Dividend history link on each component here:

Click on above image to go the dividend history pages.

Dividend History page links for a few components are listed below:

Disclosure: No Positions