The Magnificent Seven have had a great run in recent years including last year. They continue to remain strong and some have shot up even further so far this year. For example, Meta Platforms (META) soared over 20% this past Friday after great 4th quarter earnings and the announcement of a dividend payment. Meta had a market cap of over $1.0 Trillion before this 20% jump. The rise of over $200 billion in market cap in a day is a record for any company in the US markets. The questions on some investors’ mind is this huge jump warranted.

Other mega caps have astonishing market caps as well with Apple (AAPL) at $2.87 Trillion and software giant Microsoft(MSFT) topping even that at over $3.0 Trillion. Similarly Amazon(AMZN), Alphabet(GOOGL), Nvidia(NVDA) and Tesla(TSLA) have huge market caps as well. With that said, let’s discuss on some of the challenges faced by these market champions and a few related articles in this post.

An excerpt from an article by Raheel Siddiqui at Neuberger Berman:

All the glitters may not keep turning to gold

The Mag 7’s achievements in 2023 notwithstanding, we fear these marquee stocks could face headwinds in the coming year.

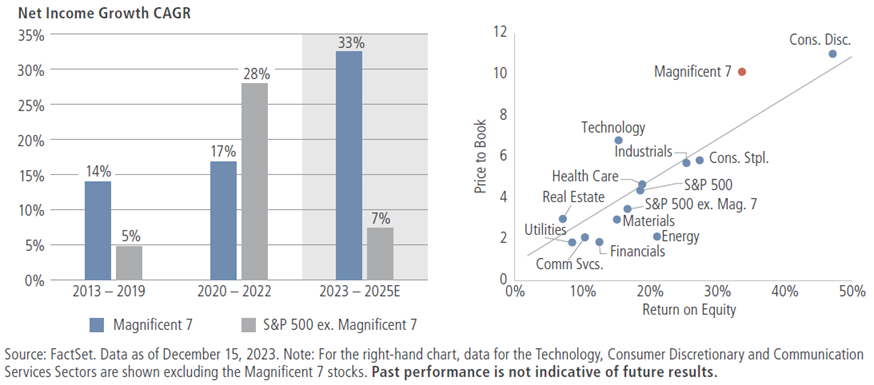

First, valuations appear precarious, in our view. Wall Street expects the Mag 7’s earnings and revenues to grow 33% and 17% per year, respectively, through 2025 (see the left chart in figure 3). Yet even considering the group’s relatively high returns on equity (shown on the right), the Mag 7 has the unnerving distinction of being the largest and most expensive grouping within the S&P 500. At current valuations, we believe this group—which now represents more than a quarter of the S&P 500—is roughly 60% more expensive on a P/E basis than the rest of the index, making them potentially vulnerable to even minor hiccups in the coming year.

Figure 3: The mag 7’s strong earnings expectations are commanding relatively rich valuations

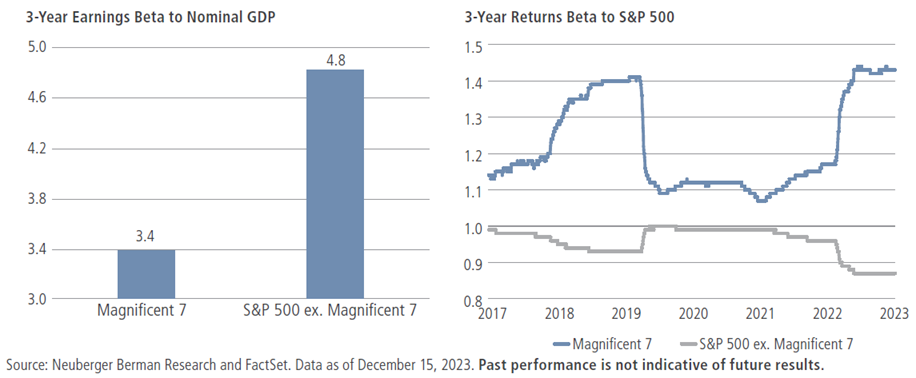

Second, the Mag 7 may prove more cyclical than investors seem to expect. These giants are often considered defensive businesses given that their products drive the relentless modernization of society, and that they also boast strong balance sheets and relatively high, stable profit margins. Indeed, over the last three years, the Mag 7’s earnings beta to nominal GDP has been 30% lower than the rest of the S&P 500 (see the left side of figure 4); however, the price beta of these stocks—at 1.4—was 50% higher than the rest of the S&P 500 (as shown the on right).

Figure 4: The Mag 7 may be less defensive than investors anticipate

Third, we believe the price returns of these seven stocks are highly correlated to each other—meaning that, from a portfolio perspective, owning them as a group is akin to inviting additional risk rather than diversifying away from it. Since 2017, the average pairwise correlation of the Mag 7 has been 55%—that’s 70% higher than for the rest of the 493 stocks.3 Furthermore, we find that correlation tends to rise during selloffs, which could make holding these stocks even riskier in a downturn.

Therefore—and despite some of their defensive characteristics—we fear that investors may have overlooked the inherent cyclicality and correlation of the mega-caps, potentially magnifying the investment risk should the Mag 7 begin to lose favour.

In addition he notes that these seven firms derive about half of their revenue from outside the US. Should the global economy go into contraction mode this will be problematic to their earnings.

And 2023 isn’t alone. Though 2022 was a break from the recent pattern, US index-tracking strategies have now beaten the combined wisdom of active investors for 8 out of the last 10 years. The scope and length of that remarkable run now eclipses even that of the dotcom boom.

Never before has following the crowd made so much money. Nor, in our estimation, so little sense. But just look at the opportunities the crowd has left for those of us willing to take a different view.

We could wax lyrical about the glaring difference in value between Korean banks priced at 4 times earnings, versus Apple at 28 times, despite diverging fundamentals—Apple is increasingly at risk of bans in China, while Korean banks could double their dividends.

Or how the thick margin of safety at Intel, backed by listed stakes and real saleable assets, compares to the slim margin for error at Nvidia, trading at 13 times next year’s projected revenue. That revenue that could be competed away over time, while Intel’s semiconductor “fabs” in the US are increasingly valuable as the east and the west drift further apart.

We could effuse about the quality of Nintendo’s innovation engine, and marvel at Mr Market’s willingness to extrapolate dominance for the Magnificent Seven while putting little value on Nintendo’s exceptional intellectual property.

But those deep dives would only cover a fraction of the portfolio, which risks diluting the message on how distorted the overall opportunity set has become.

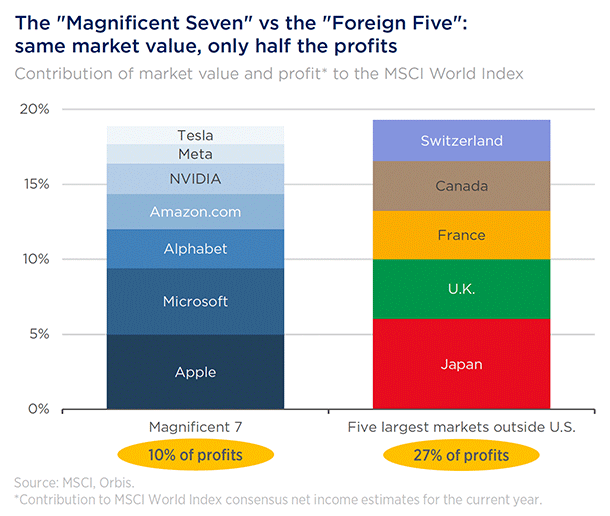

Not since the inception of the first Orbis Funds in 1990 has one country’s benchmark weight punched so far above its share of global GDP (then Japan, now the US). Nor since our sister company Allan Gray’s creation in 1973 have a handful of shares commanded such a large proportion of the market. Today, the Magnificent Seven stocks command as much market value as the “Foreign Five”, the largest developed stockmarkets outside the US by market value, yet the Seven contribute less than half the profits of those stockmarkets.

Niels Clemen Jensen at Absolute Return Partners, UK also wrote in the latest edition of The Absolute Return Letter that the mega caps are expensive and they have made the US market also expensive in terms of valuations.

It remains to be see how the rest of the year turns out for the magnificent seven stocks.