Infrastructure is one of the key sectors that will see large investment as part of the massive $787 billion package signed President Obama last month. The law titled “American Recovery and Reinvestment Act” will promote investment in infrastructure such as roads, bridges, electricity grid, etc. Billions of dollars will pour into these projects over the next months.

But is this infrastructure spending necessary now? Will it help revive the long-term economic growth?.

According to the Organization for Economic Cooperation and Development (OECD) spending on infrastructure projects will be beneficial for long-term prosperity. Yesterday March 3rd, the OECD released the Going For Growth 2009 report. This flagship “annual periodical provides an overview of structural policy developments in OECD countries from a comparative perspective.” In this report, Klaus Schmidt-Hebbel, the Chief Economist says that infrastructure performs a vital role in the functioning of our economy. However in the past, some investments made in this sector have been wasteful.

The report identifies many policies that can “both boost demand in the short term to soften the impact of the recession, and also raise economic growth over the long term. This ‘double dividend’ can be achieved by pursuing policies areas such as:

- Increased spending on infrastructure

- Increased spending on active labor market policy

- Reduction of personal income taxes

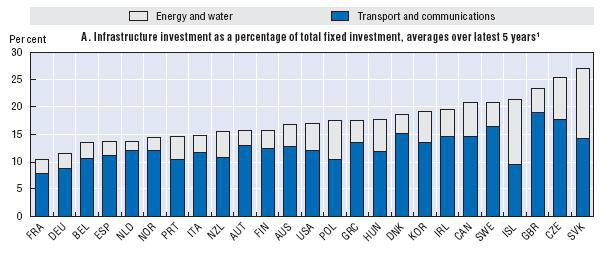

Charts – Investment in Infrastructure Sectors (click to enlarge)

A)Infrastructure Investment as a % of Total Investment

The above diagram shows that the USA has lagged in infrastructure spending on energy and water, transport and communications in the last 5 years when compared to other OECD countries such as Sweden, Denmark, Korea, Great Britain, etc.

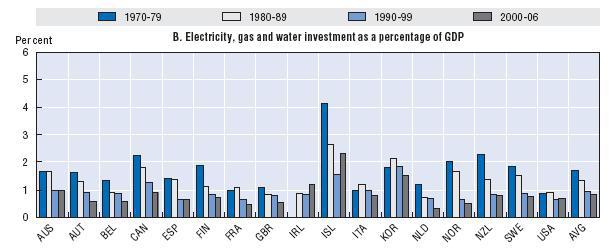

B) Electricity, Gas and Water Investment as a % of GDP

In the years 2000-2006, we spent below the average in electricity, gas and water investment as a % of GDP. Less than 1% of the GDP went into these areas. Sweden, Norway, Israel, Korea, Ireland spent more than USA in these sectors during the time period. The US invested a higher portion of the GDP during the 70s and 80s but has slipped in the past few years.

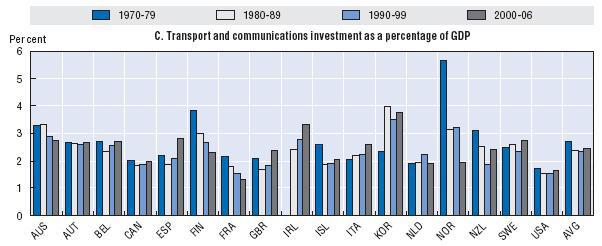

C) Transport and Communications Investment as a % of GDP

Source: OECD -Going For Growth 2009

Investments in transport and communications were less than the average of all OECD countries during 2000-06. Only France spent less than us in the same period. Many countries such as Austria, Australia, Sweden, Korea, Spain spent a larger portion of their GDP on these two sectors.

In summary, from the above three charts it is clearly evident that infrastructure spending needs to be increased in the US. The OECD report mentions that investment investments may have positive spillovers throughout the other parts of the economy. But to reap the full benefits of such investments, it is essential to carefully select projects that will deliver the most benefits. Furthermore strong regulatory measures must be in place to ensure competition among market players in executing the projects. While I agree with Klaus Schmidt-Hebbel on the “double dividend” theory it is not 100% sure that infrastructure spending will revive growth in the US. This is due to the fact that the US economy was mostly supported by the consumer spending. It is unlikely that the consumer will start spending again with just because of all the new roads, bridges, schools, green buildings, etc.However in the long-term having high-quality infrastructure will promote sustainable growth and improve the standard of living.