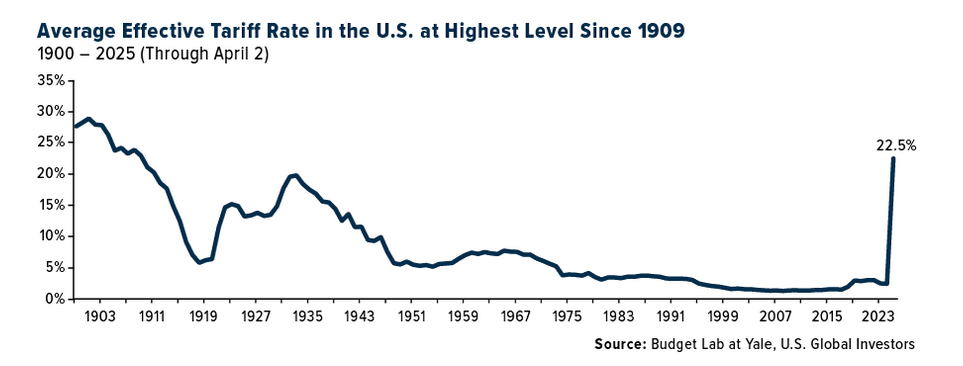

The US average effective tariff rate has reached the highest level since 1909 with the raft new tariffs announced by President Trump according to Yale Budget Lab. According to their estimates, the rate has reached 22.5%. Frank Holmes at U.S. Global Investors notes 1909 is the year President Howard Taft proposed the idea of an income tax to Congress !

Click to enlarge

Source: America’s Tariff Rate Hits the Highest Level Since 1909—And That’s Before Retaliation, U.S. Global Investors

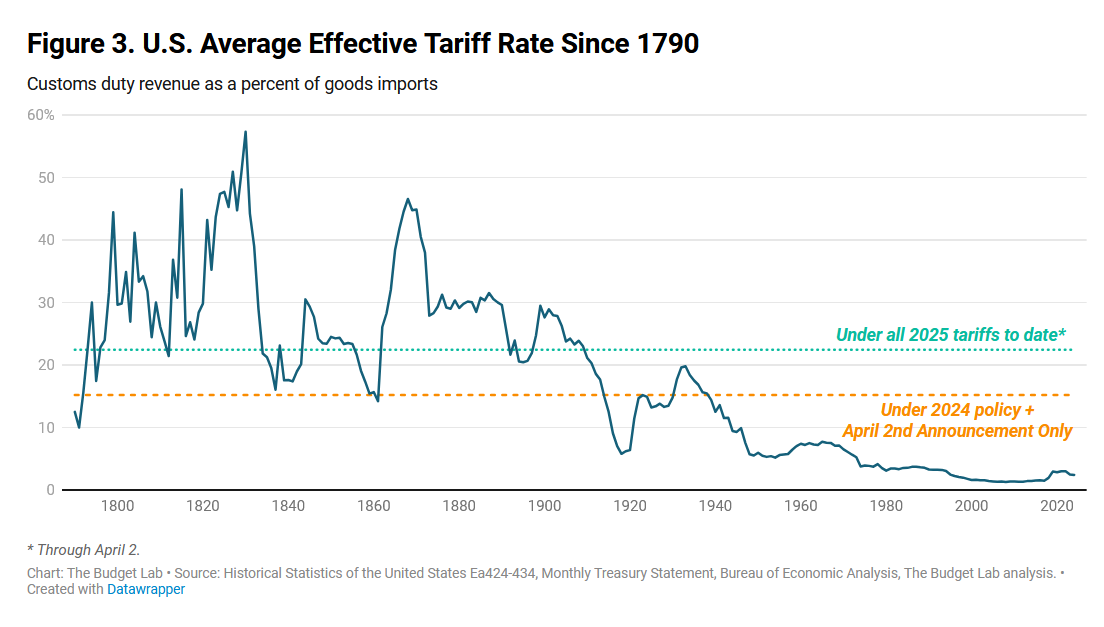

The US Tariff rate was much higher back in 1800s and up to early 1900s. However back then concepts like globalization were not a thing. So it is not wise to compare current rates to the rates in those years.

Click to enlarge

Source: Where We Stand: The Fiscal, Economic, and Distributional Effects of All U.S. Tariffs Enacted in 2025 Through April 2, The Budget Lab, Yale University

While China has quickly retaliated, it remains to be seen how other countries take action to deal with the tariffs announced by the US.

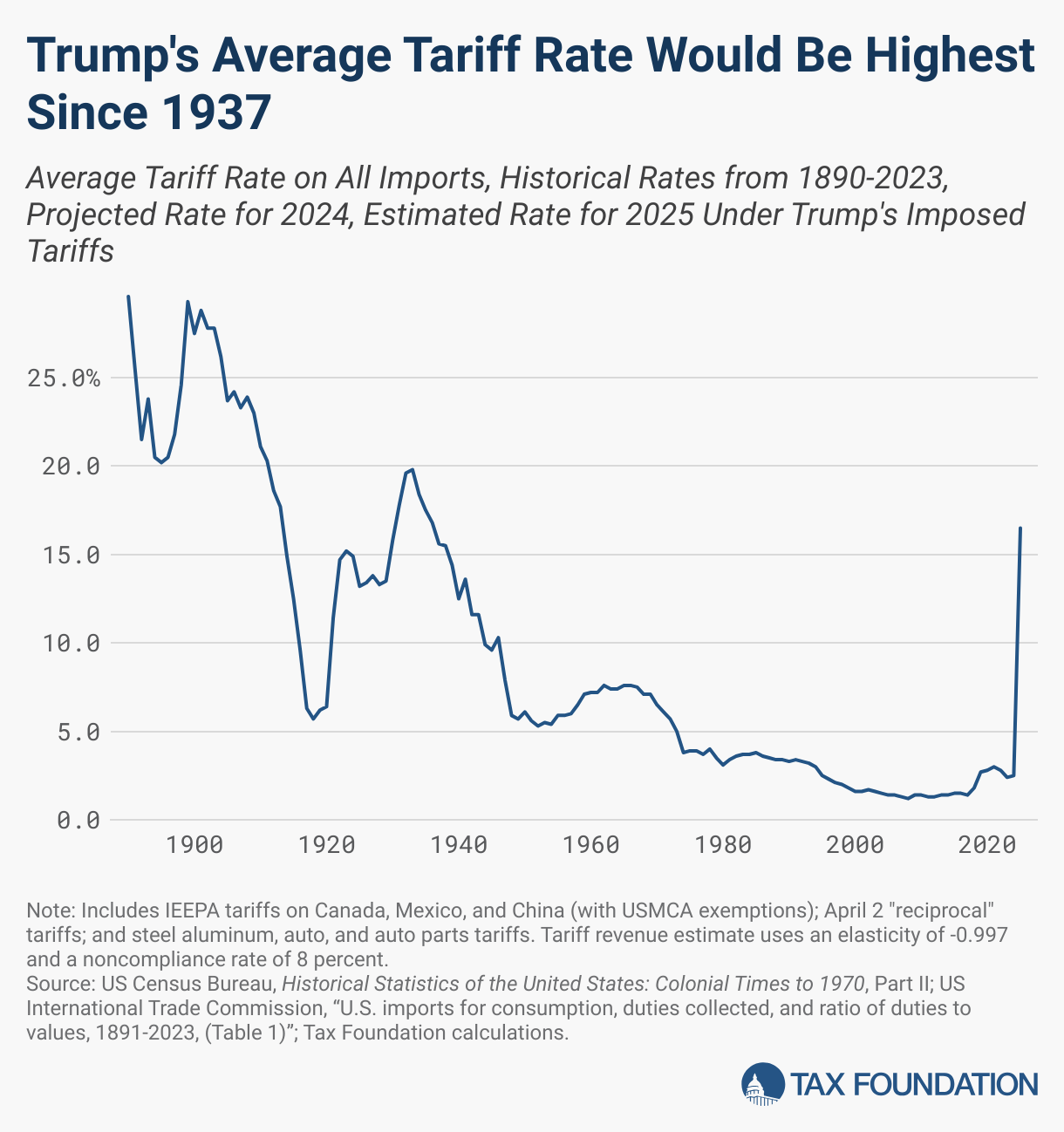

Update (4/5/25):

1.Trump’s Average Tariff Rate would be highest since 1937:

Click to enlarge

Source: Trump Tariffs: The Economic Impact of the Trump Trade War, Tax Foundation

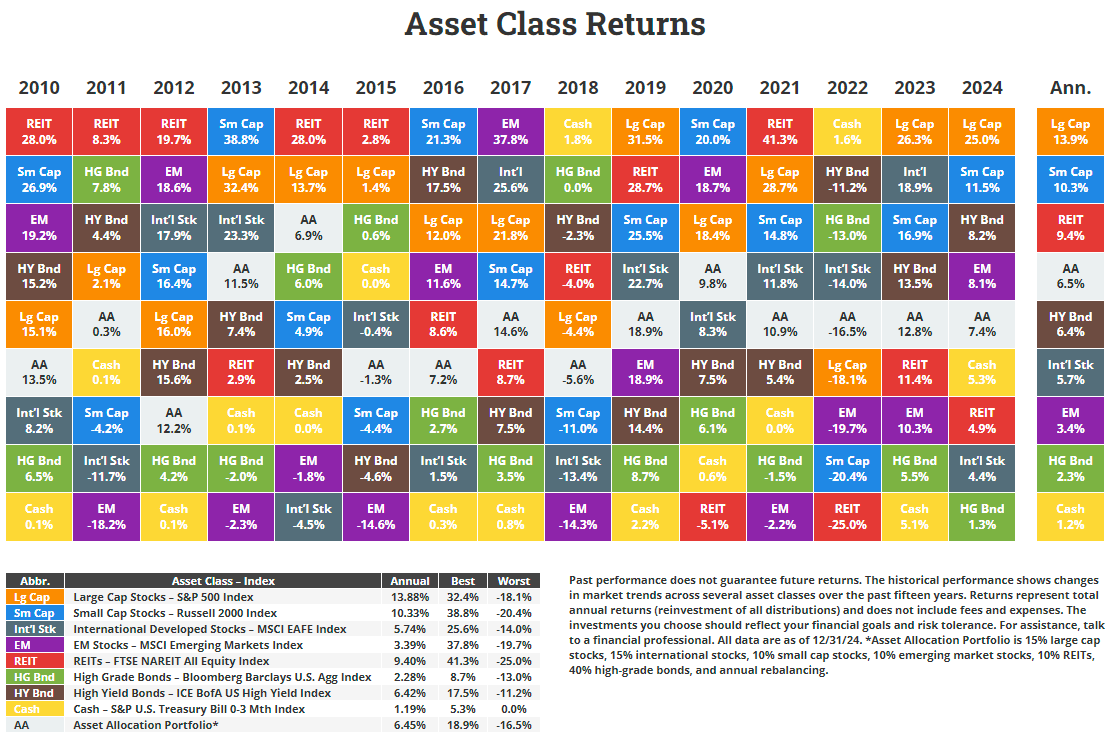

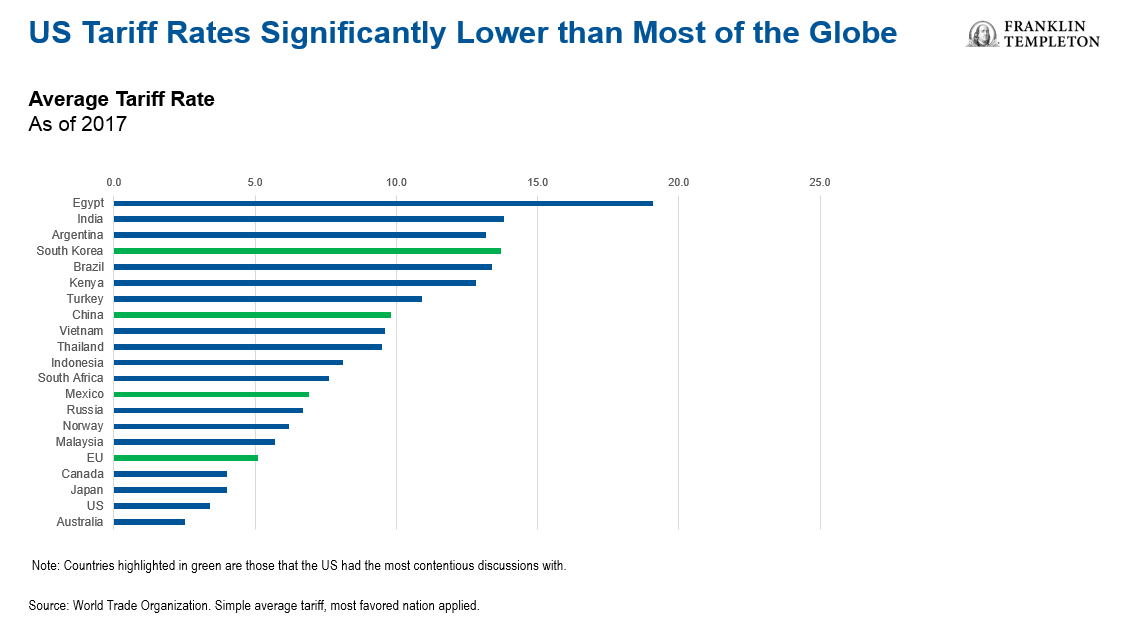

2.From an earlier post in 2019:

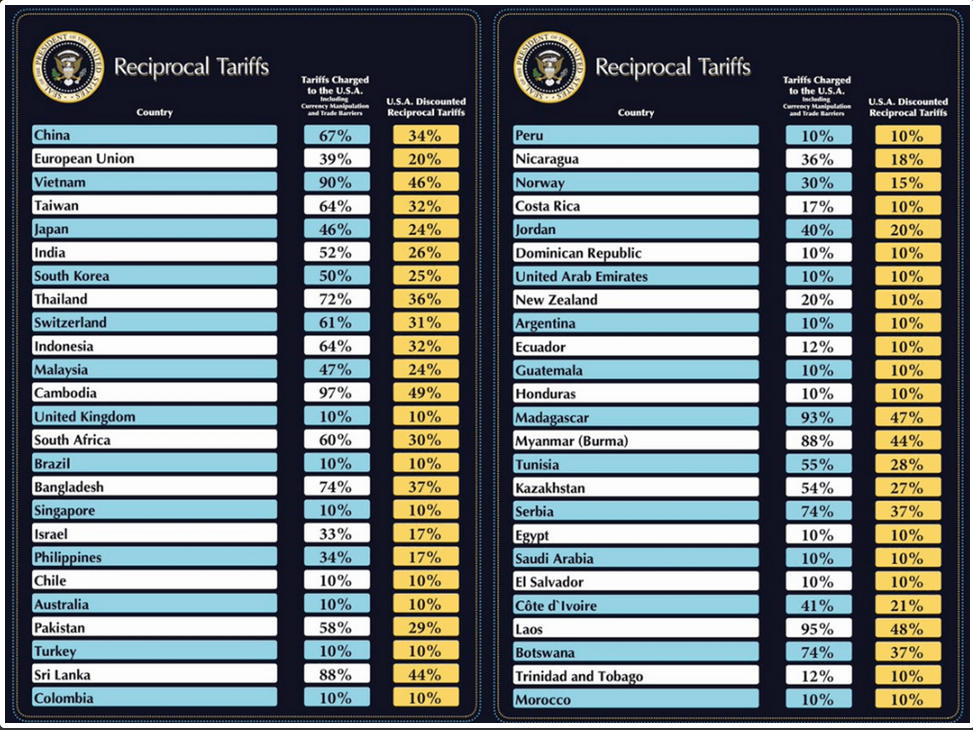

3.Trump’s Reciprocal Tariff Rates 2025:

Source: via Thinking out loud, Syz Private Banking