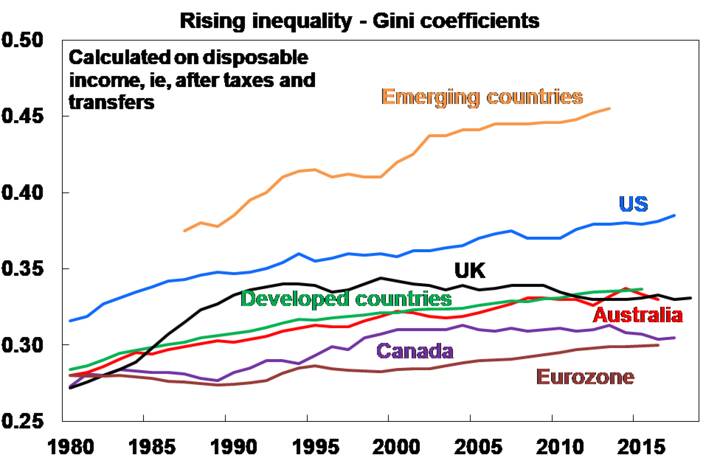

Inequality as measured by the Gini coefficients is the highest in emerging countries. Among developed countries, the US has the highest inequality which is not surprising. Inequality is also rising in the US due to a variety of reasons including tax cuts for the wealthy, lower tax rates on capital gains over labor income, etc.

Click to enlarge

Source: Five reasons why I am not so fussed about the global outlook by Dr.Shane Oliver, AMP Capital