The bull market in US stocks continues to move ever higher. After a short lull during the summer months and big decline last year, investors are bidding up tech stocks like there is no tomorrow. Artificial Intelligence(AI) is just one of the latest technological innovations that is driving these stocks. However investors have to remain cautious and keep an eye on the exit when they fall out of favor. A few articles I read this weekend hi-lighted the growth of this sector and discussed if they are warranted.

Before we get to those articles, for perspective the NASDAQ composite is up by 35% YTD. But the NASDAQ-100 index which constitutes the 100 largest non-financial companies in the NASDAQ have soared by 45% YTD.

Below is an excerpt from an article by Charles-Henry Monchau at Syz Group:

According to the Bank of America chart below, the Nasdaq has reached an all-time high relative to the S&P 500. The current surge has eclipsed the highs of the Internet bubble of 2000 and the peak reached during the bull market of the 1960s. (emphasis mine)

The current boom in the technology sector is fuelled by the very optimistic outlook for artificial intelligence. Will AI deliver on all its promises, or will we soon see a 2001-2002-style backlash?

The Economist magazine published a fascinating article recently titled “Forget the S&P 500. Pay attention to the S&P 493”. From the article:

Think of america’s stockmarket. What is the first firm that springs to mind? Perhaps it is one that made you money, or maybe one whose shares you are considering buying. If not, chances are you are thinking of one of the big hitters—and they don’t come much bigger than the “magnificent seven”.

Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla are Wall Street’s superstars, and deservedly so. Each was established in the past 50 years, and five of them in the past 30. Each has seen its market value exceed $1trn (although those of Meta and Tesla have since fallen, to $800bn and $700bn respectively). Thanks to this dynamism, it is little wonder that America’s stockmarket has raced ahead of others. Those in Europe have never produced a $1trn company and—in the past three decades—have failed to spawn one worth even a tenth as much. Hardly surprising that the average annual return on America’s benchmark s&p 500 index in the past decade has been one-and-a-half times that on Europe’s Stoxx 600.

There is just one problem with this story. It is the hand-waving with which your columnist cast the magnificent seven as being somehow emblematic of America’s entire stockmarket. This conflation is made easily and often. It is partly justified by the huge chunk of the s&p 500 that the magnificent seven now comprise: measured by market value, they account for 29% of the index, and hence of its performance. Yet they are still just seven firms out of 500. And the remaining 98.6% of companies, it turns out, are not well characterised by seven tech prodigies that have moved fast, broken things and conquered the world in a matter of decades. Here, then, is your guide to the s&p 493.

The above clearly shows the huge gap in returns between the top seven and the rest of the firms in the S&P 500 index.

The next article on this topic comes from Firstlinks, Australia. From the article by James Gruber and Leisa Bell:

Last year, everyone seemed to have recognized that the prices of many assets had become ludicrous and that their subsequent pummelling was long overdue. However, a number of these same assets have come roaring back to life this year and there’s been barely a peep.

Bitcoin hasn’t not nearly got the same attention and it’s rocketed 135% in 2023. Tech stocks in the US aren’t far behind. Tech bellwether, the NASDAQ, is up a blistering 45% year-to-date. Of the S&P 500, seven stocks aka ‘The Magnificent Seven’ have risen 68% this year, while the remaining 493 stocks in the index are just 2.5% higher.

Here are ‘The Magnificent Seven’ total returns this year:

Nvidia (NVDA) +230%

Microsoft (MSFT) +55%

Apple (AAPL) +44%

Meta (META) +171%

Alphabet (GOOGL) +50%

Amazon (AMZN) +70%

Tesla (TSLA) +74%

At first glance, what’s staggering is how much the prices of these mega-cap companies have moved in one year. Apple and Microsoft are worth US$2.9 trillion and US2.7 trillion, and they’re up 44% and 55% respectively this year. For Microsoft, the market believes that the company is worth around US$950 billion more now than it was at the start of the year. Even with the hype around artificial intelligence, business values moving around this much are difficult to fathom.

Though, perhaps not. Let’s look at the trailing price-to-earnings (PER) multiples of the seven stocks, based on Morningstar estimates:

Nvidia 117x

Microsoft 36x

Apple 30x

Meta 29x

Alphabet 25x

Amazon 75x

Tesla 72x

Simple average 55x

The simple average multiple of 55x compares to the S&P 500’s 24x, a premium of 129%.

Of course, some of the stocks above are set for stellar growth over the next few years. Nvidia, riding the AI boom, is a standout here.

Yet other stocks with high multiples attached are struggling to grow. Apple is one. Another is Tesla where Morningstar expects earnings to shrink this year as competition heats up in the electric vehicle space. And Alphabet faces a serious structural threat to its dominant search engine business from AI.

Have earnings driven stellar tech returns?

I thought it would be a worthwhile exercise to look at how much earnings growth has contributed to the rise in share prices for some of these stocks. For instance, Microsoft’s stock has risen by 861% over the past decade. That’s excluding dividends. Including those, and the stock has compounded at 26% per annum. A stellar performance.

How much of that performance was driven by earnings? Well, earnings per share over that period increased at a compound annual growth rate (CAGR) of 14% on revenue which grew at an 11% CAGR clip. In simple terms, earnings accounted for a little over 50% of the Microsoft’s price rise over the 10 years. The remaining 50% or so came from expansion in the multiple attached to the stock.(emphasis mine)

Back in 2013, Microsoft was considered a stodgy dinosaur and it was valued as such, bottoming with a trailing PER of 13x. How times have changed.

For Apple(AAPL) about 40% of the total return over the past 10 years can be attributed to expansion in earnings multiple.

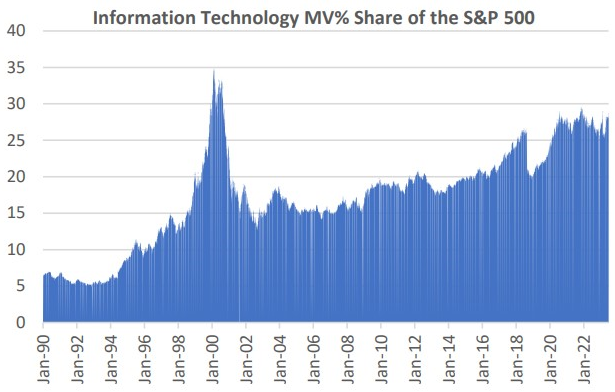

Here is another excerpt which shows that the weighting of the tech sector now has exceeded that of the level reached in 2000.

S&P 500 tech weighting also flashes warning sign

It’s not only the prices of large cap tech stocks that should concern investors. IT’s weighting in the S&P 500 provides further evidence of irrational exuberance in the sector.

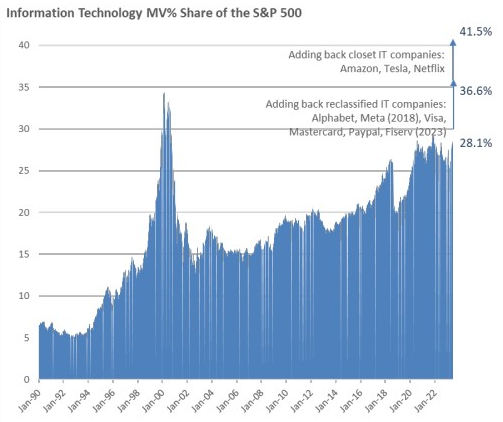

On the face of it, the tech sector’s weighting of 28% in the S&P 500 looks high.

But that doesn’t tell the full story. There are companies that should be part of the tech sector but aren’t. For example, Amazon and Tesla are classified as consumer discretionary when they’re arguably not. Amazon’s cloud business generates 107% of operating profits, which should make it an IT company. In case you’re wondering, Amazon’s online retail business doesn’t make any money (those deliveries are loss makers, after all). Netflix, Alphabet, and Meta are classified as communication companies when they clearly shouldn’t be.

If you include these companies in the tech sector, the true weighting of IT in the S&P 500 is closer to 41%, which is well above the peak of 35% reached in 2000.