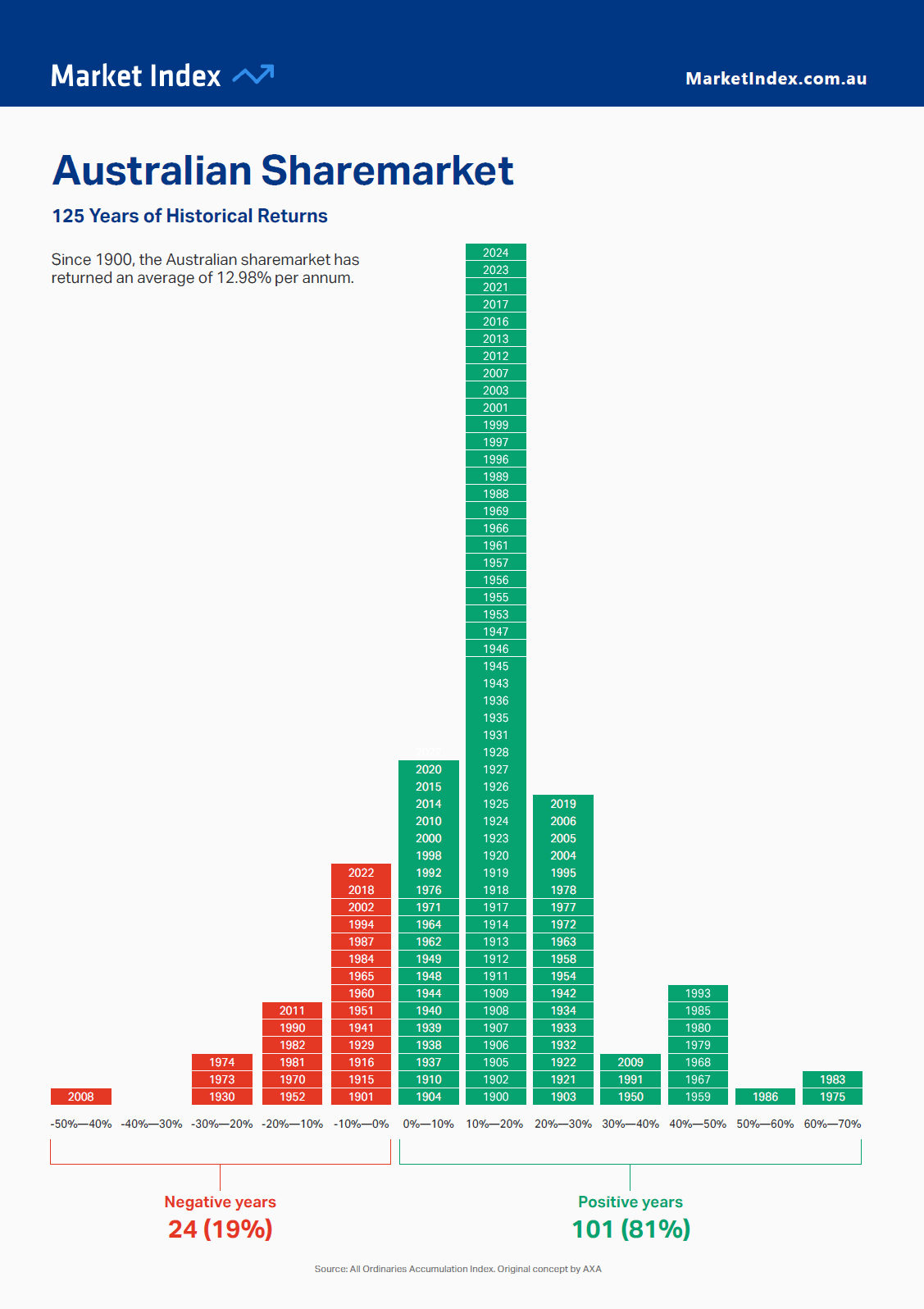

Investing in emerging markets is riskier than investing in developed markets. One way to reduce risk and still gain from these markets is by diversifying part of one’s portfolio among a bunch of emerging markets. The best performing market in one year can easily become the worst next year. The following annual returns chart for emerging markets from 2011 to 2025 from Novel Investor shows this figuratively. For example, Turkey was the best performer in 2022 with a return of over 91%. However the following year, it was one of the worst with a loss of 3.5%. Hungary which was the worst market in 2022 turned into the best market in 2023 with a gain of over 50%.

In 2025, Colombia had the highest return at over 115% followed by South Korea. Colombian stocks are on a tear this year also. For instance, the year-to-date returns of a few exchange-listed Colombian ADRs are shown below:

Grupo Cibest S.A. (CIB): 28.36%

Grupo Aval Acciones y Valores (AVAL): 18.77%

Ecopetrol (EC): 25.45%

Note: Returns shown above are excluding dividends and thru Jan 30,2026.

The Colombian equity market is rising this year as many Colombian firms are expected to benefit from the improving political situation in Venezuela.

Click to enlarge

Note: The returns shown above are total returns that include dividends reinvested. And the returns are based on the MSCI indices for each country.

Source: Novel Investor

For an interactive version of the above chart, click on the link above.

Related ETFs:

- The Global X MSCI Colombia ETF (COLO)

- WisdomTree India Earnings (EPI)

- The iShares MSCI India ETF (INDA)

- iShares MSCI Mexico Capped Investable Market (EWW)

- iShares FTSE/Xinhua China 25 Index (FXI)

Disclosure: Long EC and CIB