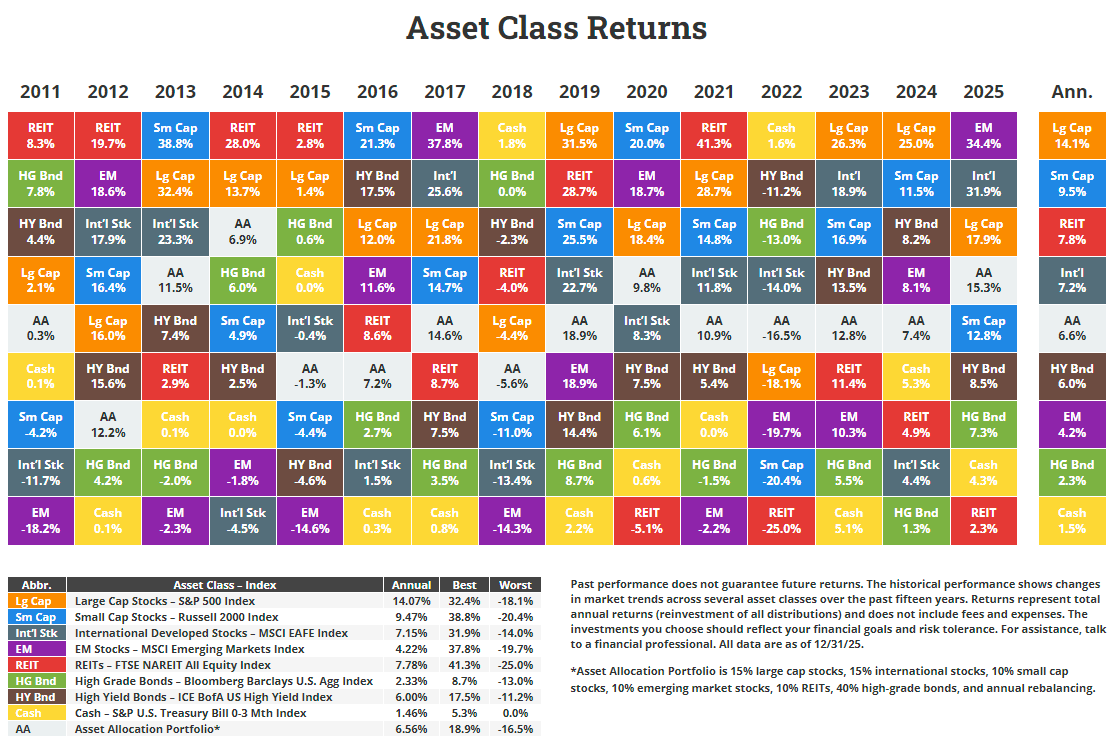

Bonds are be an integral part of a well diversified portfolio. While equities can generate amazing returns when equity markets are booming but can decline when markets turn south. Bonds on the other hand, tend to earn average returns when bonds markets do well and their negative returns during other times are low. In addition, fixed income assets such as bonds provide a cushion effect to a portfolio when equity markets crash.

The following chart shows the Average Annual Returns for US Bonds by Calendar Year 1926 to 2025:

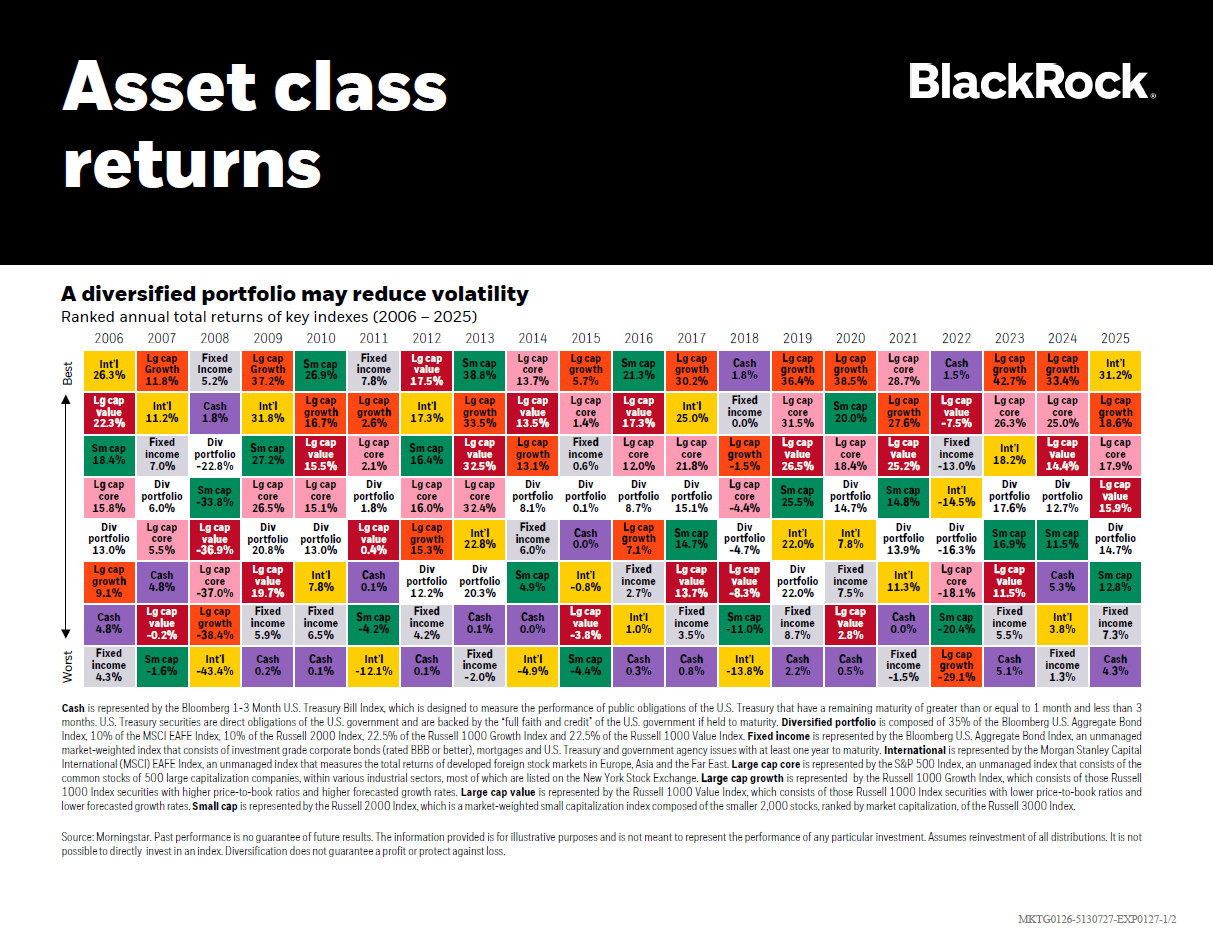

Click to enlarge

Source: Student of the Market-January 2026, Blackrock

In 2025, US bonds performed very well relative to their average returns. Bonds can also earn amazing returns as shown above during the 12 years when they yielded over 10%.

Related ETFs:

- iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD)

- Vanguard Total Bond Market ETF (BND)

- SPDR® Barclays High Yield Bond ETF (JNK)

- iShares Core Total U.S. Bond Market ETF (HYG)

- iShares TIPS Bond ETF (TIP)

Disclosure: No positions