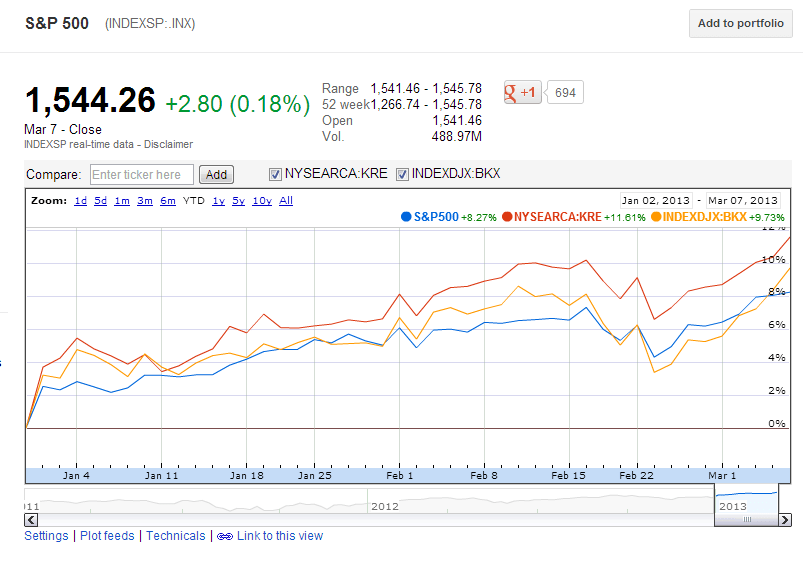

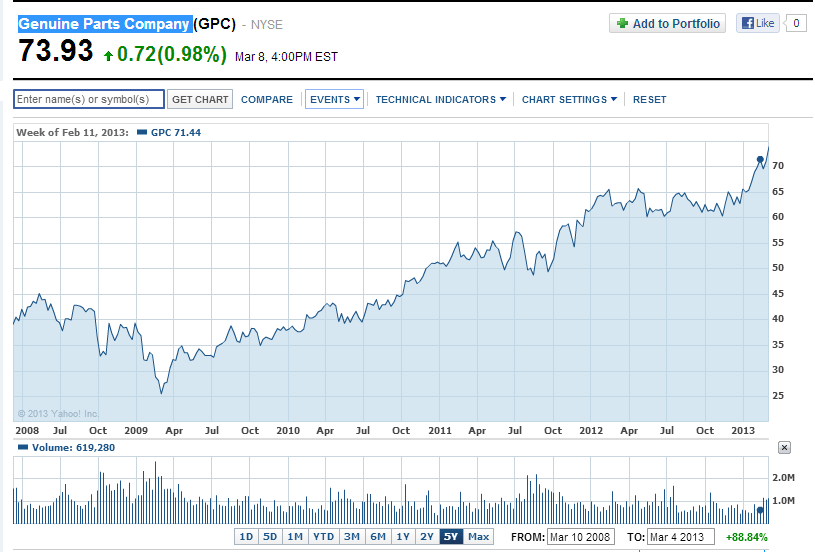

I wrote about auto parts makers back in January. Among the five big companies in this industry Genuine Parts Company(GPC) reached a 52-week high last week. From a low of about $25.00 in March 2009, the stock reached over $74 last week as shown in the chart below:

Click to enlarge

Source: Yahoo Finance

The company has over $11.0 B in market cap and has a current dividend yield of 2.91%. Other auto parts makers such as Magna International of Canada (MGA) also reported strong earnings recently. As auto sales have picked up since the credit crisis lows and continues to grow, auto parts makers are bound to grow as well. Hence despite the 52-week high GPC and others are worth adding at current levels.

It is interesting to note that GPC is one of the top holding in The AdvisorShares Global Alpha & Beta ETF (NYSE: RRGR) which is run by fellow blogger and portfolio manager Roger Nusbaum, CIO of Your Source Financial.

Note: Dividend yields noted are as of Mar 1, 2013

Disclosure: No Positions