Why BlackBerry failed (The Guardian)

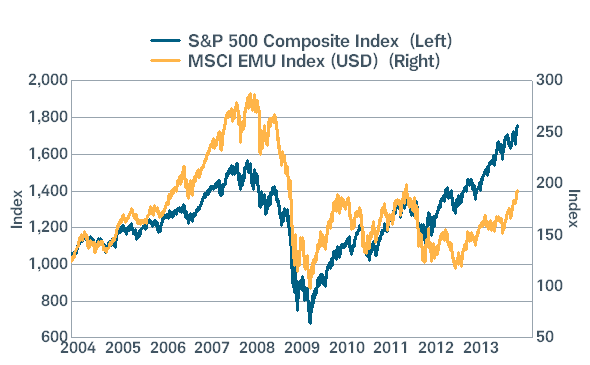

Canada vs. U.S.: A tale of two stock markets (The Star)

Is now the ideal time to get back into emerging markets? (Trustnet)

World’s Safest Emerging Markets Banks in Central & Eastern Europe 2013 (Global Finance)

Bernstein Says ‘Great Rotation’ of Bonds to Stocks Flawed (Bloomberg)

From financial market deregulation to fragmentation: Ladies and gentlemen, you screwed up (OECD Insights)

What if foreign holders dumped U.S. Treasuries? (Canadian Investment Review)

Understanding Emerging Market Banks: A new eBook (Vox)

Do multinationals that expand abroad invest less at home? (Vox)

Kuala Lumpur, Malaysia