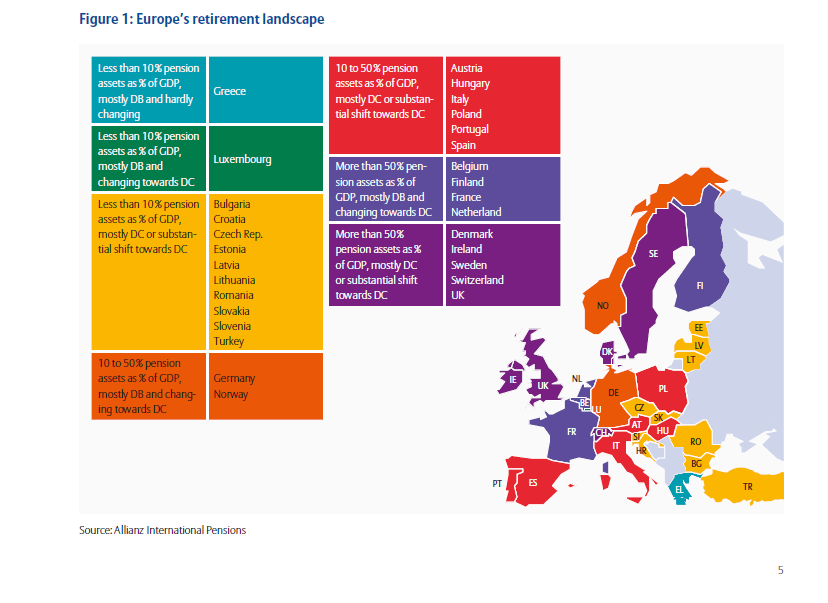

Retirement plans in European countries are slowly changing in recent years. Countries are moving away from Defined Benefit (DB) plans to Defined Contribution(DC) plans.

In DB plans an employer basically defines a benefit that the employee will receive at a certain date in the future usually after retirement. This is usually a set amount based on the employees wages, tenure, etc. Once the employee retirees the employer pays the defined amount(called as pension) periodically to the employee. Here the employer is responsible for the risk associated with managing the funds of employees in order to make sure enough funds are available to pay to the retirees.

In DC plans, an employee contributes a certain percentage of his/her income to the plan.Sometimes the employer may also contribute a small percentage to that plan usually based on the employee’s salary and tenure.The funds of the plan are then invested in the market mostly in mutual funds already pre-selected by the employer. In this type of plan, the employee is responsible for the investment risk.

In the U.S. most companies got rid of the DB plans in favor of DC plans in the past few decades since it makes the employee responsible for their retirement and reduces the liability for companies.

Unlike the U.S., most of Europe still have DB plans. But that is changing with the increasing adoption of DC plans.In Europe, strict regulations and resistance from workers have prevented employers from quickly dumping DB plans and implementing DC plans. However since DC plans not only reduces employers’ liability but also affords employees the opportunity to earn more with their investments, they will be embraced by more employers.

The graph below the current retirement landscape in Europe:

Click to enlarge

Source: Cross-Border Defined Contribution Plans in Europe, Alliance Global Investors

The graph shows that the adoption of DC plans is not even among the countries.For example, DB plans are more prevalent in Greece and it is not changing towards DC plans. However countries such as Denmark, Ireland, UK, Sweden and Switzerland have large portion of DC plans compared to other countries.