The Unemployment Rate in the US stood at 4.7% according to the BLS. The long-term term in unemployment since 1999 is shown in the chart below:

Click to enlarge

Source: BLS

Since the peak of the Global Financial Crisis unemployment level has slowly declined to reach almost closer to the 1999 levels. However most workers don’t feel like it is 1999 and competition is still fierce for any job open.

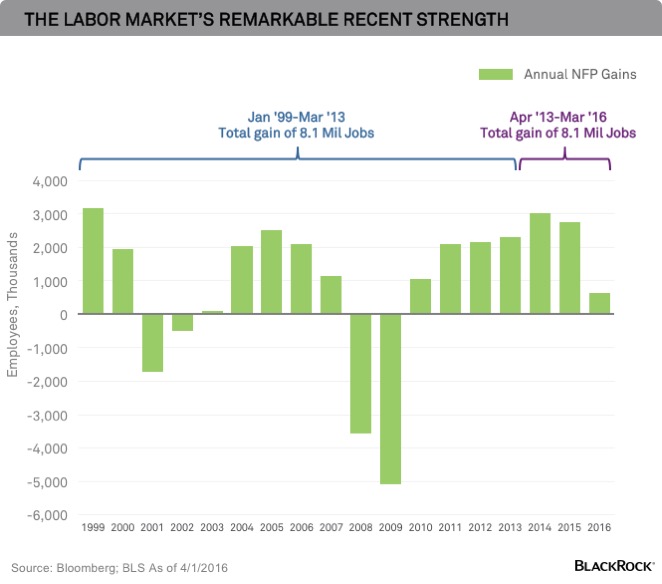

According to one expert at Blackrock, most people have missed one great statistic on the US economy. From an article published in April by Rick Rieder:

Many commentators seem to be pessimistically focused on the U.S. economy’s weak wage growth and manufacturing sector trouble. They don’t appear to be paying attention to the signs that the U.S. economy has actually been operating at a very high level in recent years, including one statistic that shows the economy’s true strength.

This statistic, which may surprise you: In aggregate, the hiring of 8.1 million people over the past three years is equal to all the U.S. job creation accomplished in the 14 years prior, according to a BlackRock analysis of jobs data following the March employment situation report. See the chart below.

In recent years, the U.S. economy has operated at much better levels than many market watchers gave it credit for. It has displayed quite remarkable labor market strength considering the secular headwinds to growth, such as an aging demographic, and it has been growing much faster than traditional metrics depict. This is because, as I’ve noted before, new technologies provide services at a much lower cost, and deliver efficiencies and productivity enhancements that are not captured in traditional economic data.

Source: A statistic about the U.S. economy that may surprise you, Blackrock Blog, April 7, 2016

So based on the charts above one can argue that all the jobs lost in the past 14 years have been recreated. But that does not tell the whole story. Millions of Americans are still looking for jobs that they lost during the great recession. Some factors that are not shown in cool looking charts like the above are things like the quality of jobs created, full-time or part-time, jobs with benefits paid or no benefits, etc. For instance, someone losing a well-paid job in a stable industry and getting a job as a hourly sales person at a department store or flipping burgers at a fast-food place for minimum wage is not the same thing.While it is true the person is employed and working, it is the quality of job that matters.

Many Americans including Presidential contender Donald Trump consider the real unemployment rate is much higher. His success in winning many state primaries confirms that many do not believe it is 1999 and everything is great. In fact, his campaign slogan is “Make America Great Again”which implies that that is average or not great now.

Here is an excerpt from an article by Barry, a fellow blogger and a Wall Street veteran on this topic:

By now, we have become almost used to a steady stream of inaccurate statements from the presumptive Republican presidential nominee. Most are not worth correcting. However, Donald Trump’s recent comments on the federal government’s unemployment data, so reminiscent of those made a few years ago by former General Electric chief Jack Welch, deserve a rejoinder. (He called today’s report that employers added just 38,000 jobs “terrible” — but only if you ignore the 35,000 striking Verizon workers. Still, 73,000 new jobs is pretty meh.)

The New York Post’s John Crudele last week interviewed Trump, who said he thinks the jobless rate is close to 20 percent and not the roughly 5 percent reported by the Labor Department. And, of course, Crudele reported, anyone who buys the 5 percent figure is a “dummy,” according to Trump.

This, in a nutshell, is typical of the usual economic conspiracy theories we have discussed in the past; it is obvious political bias corrupting economic analysis. It plays upon people’s recent post-traumatic stress from the financial crisis first and exploits their anxiety about the future. It also reveals deep ignorance about how employment data is assembled.

Source: Trump Finds Cooking in the Unemployment Numbers, Barry Ritholtz, June 2, 2016, Bloomberg

In summary, if one believes the official figures then probably so many millions of jobs have been created in recent years. Otherwise it is a fiction.