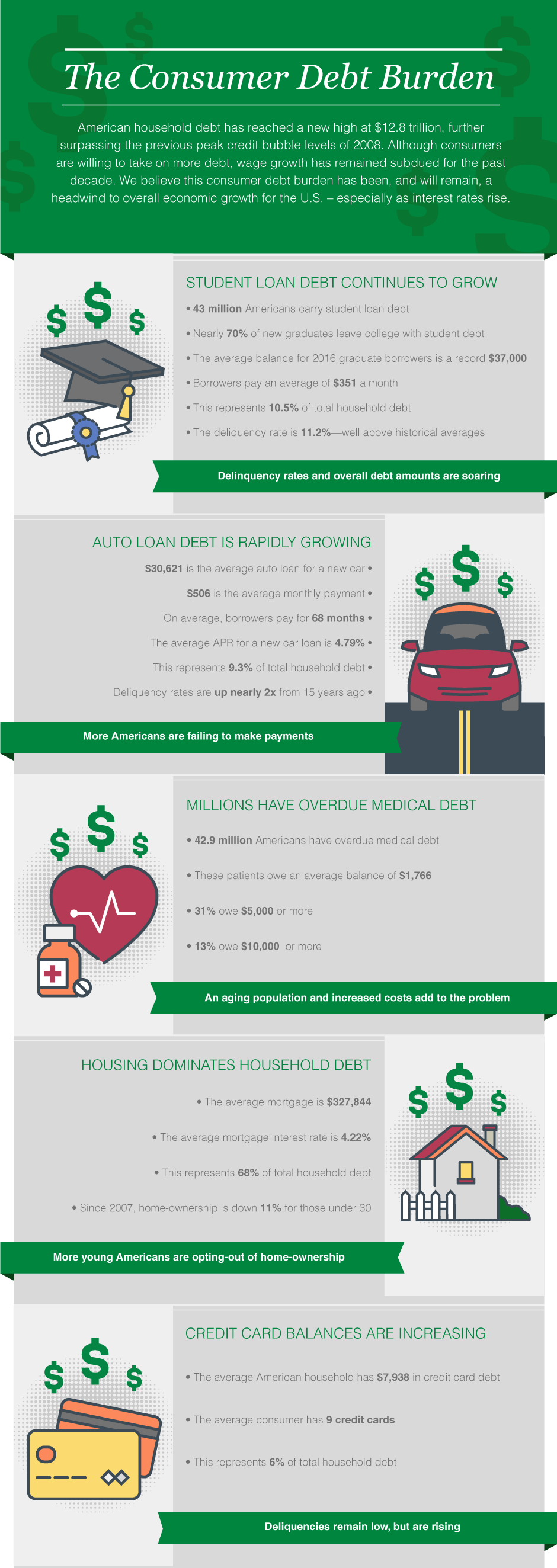

The US unemplyment rate stood at 4.4% in August according to BLS data. Despite the steady decline in the rate since the Global Financial Crisis(GFC) wage growth contniues to be stagnant. In most industries wages have not kept up with inflation. However the economy as a whole is growing due to credit markets. Debts of all types are soaring as workers maintain their lifestyle with debt as opposed with income.

While there are a multitude of reasons for the lack of growth in wages, one of the primary factor for low-level workers is illegal immigration. Since supply of labor exceeds demand wages tend to be sticky. According to an article at FP, native-born citizens not only earn lower wages but also pay higher taxes when illegals get benefits. From the article:

A century and more ago when the captains of American industry imported European workers for their mines, mills and factories, labour wasn’t cheap — American workers then earned the highest wages in the world — and it wasn’t subsidized. America’s industrialists would finance their recruits’ voyage by sea, and also provide the necessities of life through what were known as company towns. Industry won, workers won, and society won through the largely free-market relationships that then ruled labour markets.

Today’s captains of industry, in contrast, profit at the expense of taxpayers, who foot much of the bill for the immigrants’ medical, schooling, housing, policing and welfare costs. The National Academies study pegs the annual cost to state and local governments at US$57 billion, or US$1,600 a year per new unskilled immigrant, and estimates that it will take 75 years before this immigrant stops being a net loss to society. The native-born American worker not only shoulders much of this cost through his taxes, he also suffers a wage hit. The $500 billion per year in lost wages, in effect, amounts to an immigration tax on the native-born worker estimated at 5.2 per cent.

Source: Why America’s elites like DACA, and so many American workers don’t, Financial Post

One way workers can protect themselves from the effects of legal and illegal immigration is to get a job in regulated industries mentioned in the article.

Also see: