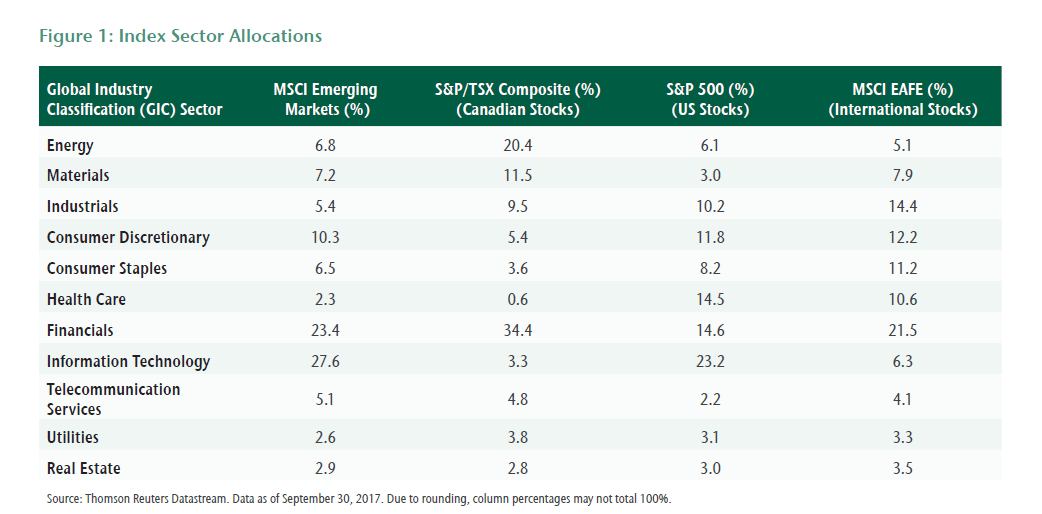

Among the major MSCI market indices, allocations to various sectors differ widely. For example, Financials account for nearly a quarter of the emerging markets index while they constitute only about 15% in the S&P 500. In Canada, financials have a higher allocation at about 34%.

The tech sector’s allocation in the EAFE and Canada’s benchmark index are very low relative to their allocation in the US and emerging market indices.

Click to enlarge

Source: CC&L Financial Group