In the modern economy, the rich keep getting richer while the poor getting poorer. Inequality in wealth and income has been growing for many decades now and the wealth disparity between the haves and have-nots is especially wider in developing countries. In many developed countries also, wealth is becoming highly concentrated with a small group of elites owning most of the wealth. Similar to developing countries, social ills like corruption, regulatory capture, favorable political and tax systems, etc. have become common in advanced countries leading to the current situation.

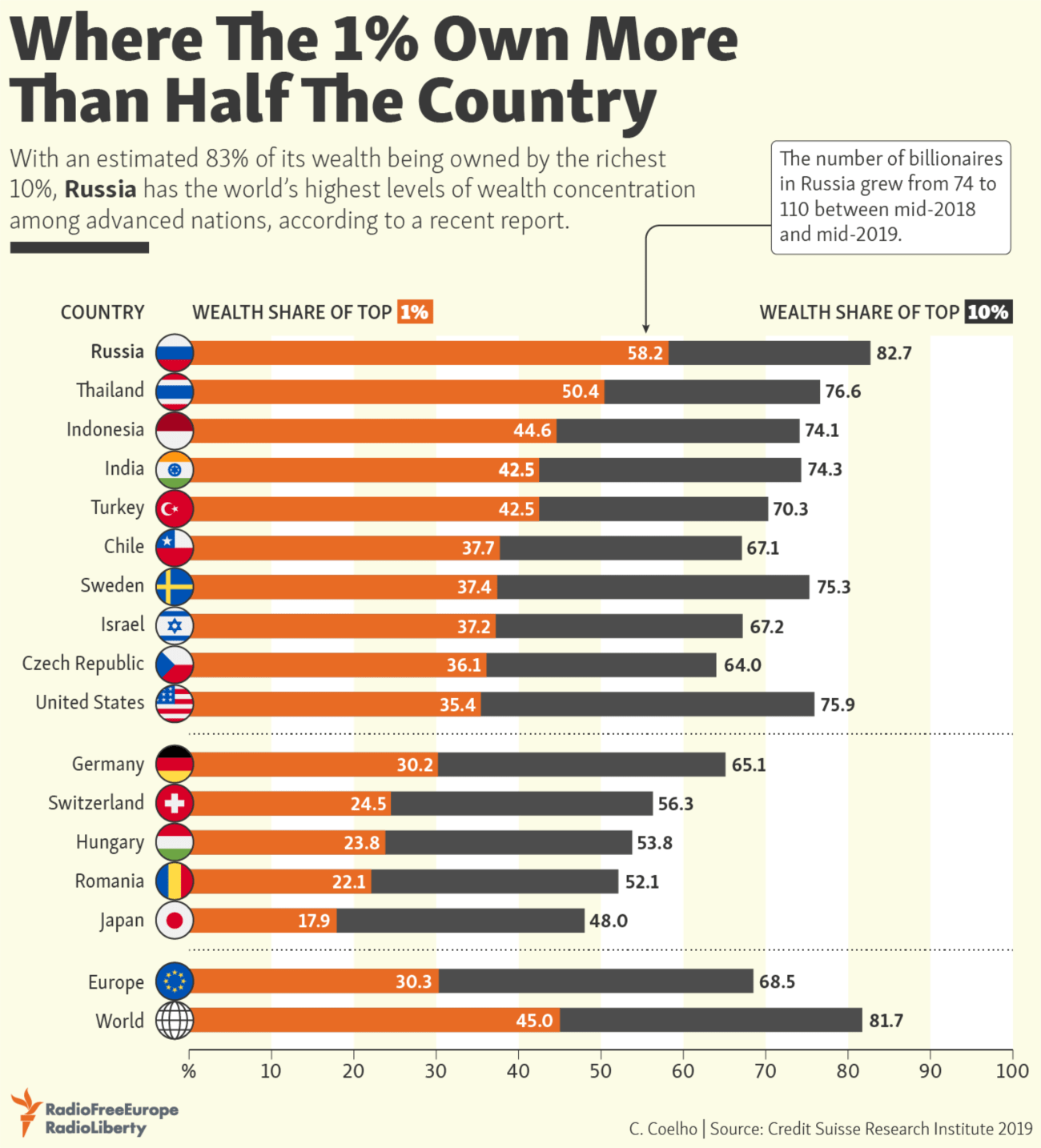

That being said, the following chart shows the share of a country’s wealth held by the top 1% and 10%:

Click to enlarge

Source: RFE/RL

Formerly communist Russia, takes the number rank for wealth concentration. The top 10% there own over 82% of the wealth with just the top 1% owing over 58% of that figure. These numbers are astonishing indeed. How times have changed !

The top six countries in this list are developing countries. India took the fourth spot. Chile which came in at number six is currently experiencing violent protests due to extreme inequality and its impacts.

In the US the top 1% owns more than one-third of the wealth.

The important question is this: If most of the wealth of a country is owned by a handful or a small group, is that a good thing for the country?