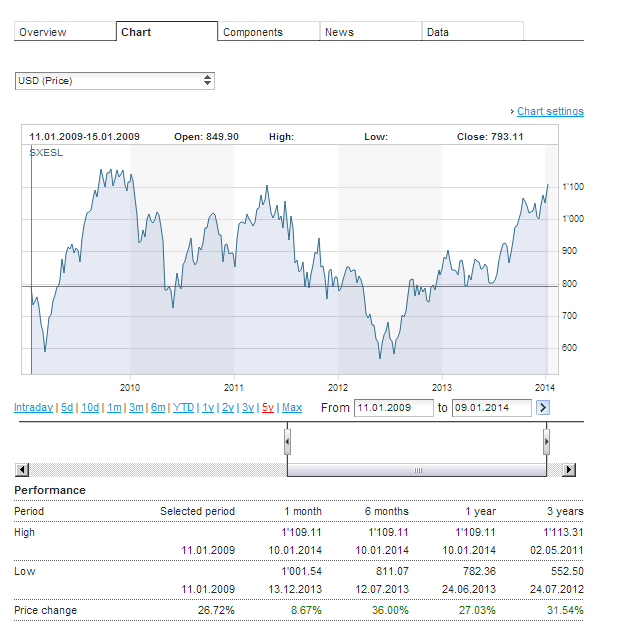

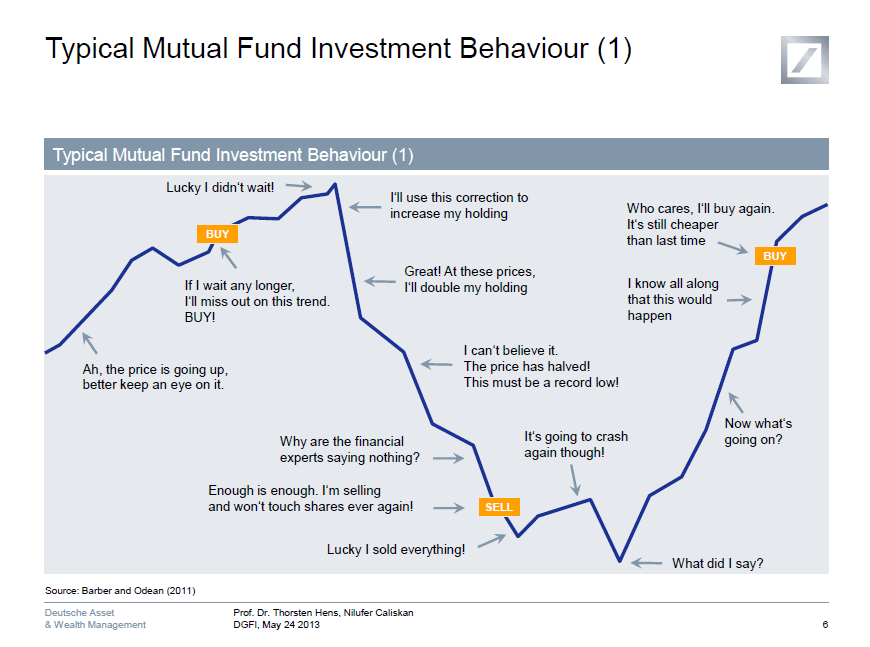

I came across the following chart showing the behavior of the typical mutual fund investor:

Click to enlarge

Source: Behavioural Finance and Mutual Fund Flows An International Study, Deutsche Asset & Wealth Management

Obviously the essence of the chart is applicable to stock and ETF investors as well.

Related:

Why We Buy in a Marked-Up Market, Jan 13, 2014, NY Times