Last week marked the 8th anniversary of the bull market that began in 2009 at the peak of the Global Financial Crisis. Since then the SS&P has soared by more than 260% with an annual average return of about 18% with dividends reinvested.

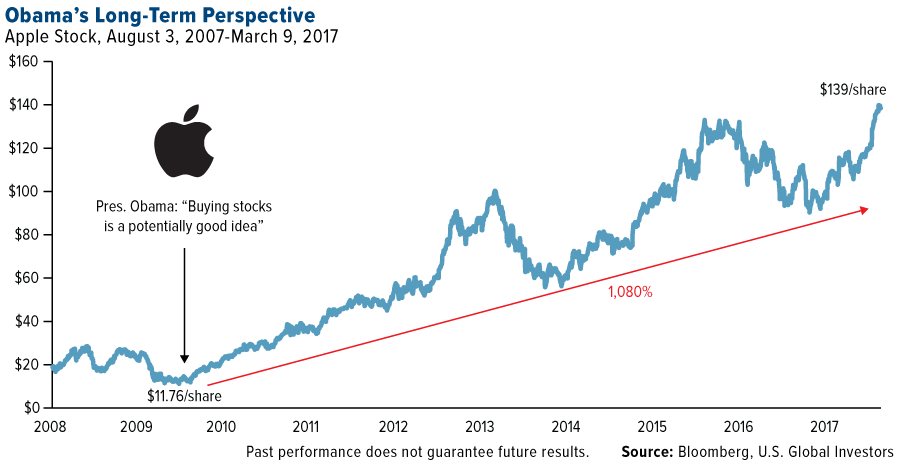

Apple(AAPL) stock has had a fantastic run that beat even the S&P 500’s 260%. Apple has surged more than 1,080 percent from early 2009 thru now.

Click to enlarge

Source: U.S. Global Investors

By any measure this is an extraordinary growth. However the question now is: Can this type of growth occur in the future? Or was this a one-time wonder that may or may not happen moving forward.

Disclosure: No Positions