FT Alphaville published an interesting analysis on why manufacturing jobs in the US are better than other jobs. The article basically debunks Gary Cohn, ex-head of the President’s National Economic Council simplistic and lack of critical thinking views on why one would prefer a nice cushy office job in an air-conditioned office than working in mine or factory which involves hard physical labor.

Manufacturing workers, though there are only about 9 million of them, make about $21.50 an hour. There are only 550 thousand mining and logging workers, but they make more than $28 an hour. They aren’t the highest-paying jobs in America, but for someone without a college degree, a manufacturing job in front of a blast furnace pays far better than an air-conditioned job inside a Target.

People in finance are famously overworked, so we’ll forgive Mr Cohn for not knowing that for many Americans, pay isn’t the only consideration. Simply getting enough hours is a challenge. Here, standing in front of a blast furnace or risking black lung (as he puts it) both have a massive advantage: both occupations offer 40 or more hours a week.

Your weekly paycheck isn’t your wage; it’s your wage multiplied by your hours. Over the last 40 years, hours overall have drifted down, particularly in retail, where in the last decade scheduling software has allowed companies to more efficiently call employees in or dismiss them. But manufacturing jobs, which are more likely to be unionised, still offer 42 hours a week. Mining and logging, which tend to run closer to capacity, offer 47 hours.

And in America, whether an employer offers benefits can make a huge difference. Last year 81 percent of production jobs offered health insurance. Overall for private workers, 68 percent. For service jobs — the single largest group — 39 percent. So the job that Gary Cohn says Americans wouldn’t choose at the same pay turns out to have better pay, better hours, and better benefits. People are nostalgic for manufacturing jobs not just because it’s nice to make something. It’s because they’re better jobs.

Another important point to be noted is that building a factory to manufacture something involves millions of dollars and machinery and takes time. Hence a company that invests so much time and effort into a manufacturing facility is not going to shutdown overnight and layoff all the workers. On the other hand, a retail joint like a department store in a mall, a coffee shop, a donut shop, a hair-style shop, a shoe shop, etc. can be shutdown overnight without any major need to dismantle machinery or other issues. So in a way the lowest paying jobs are also most vulnerable to disappear any day. This is one more reason why people yearn for manufacturing jobs than a retail job.

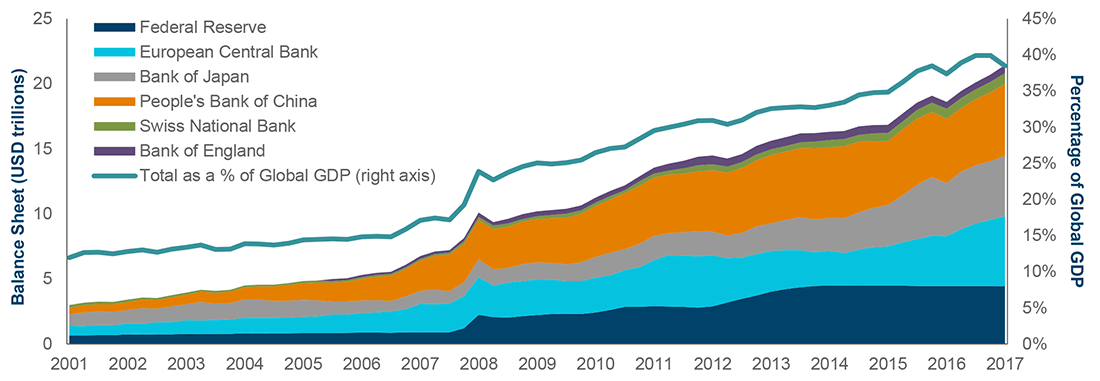

The balance sheets of major global central banks have steadily increased since the Global Financial Crisis of 2008-2009. The chart below shows the balance sheet figures measured against the percentage of Global GDP:

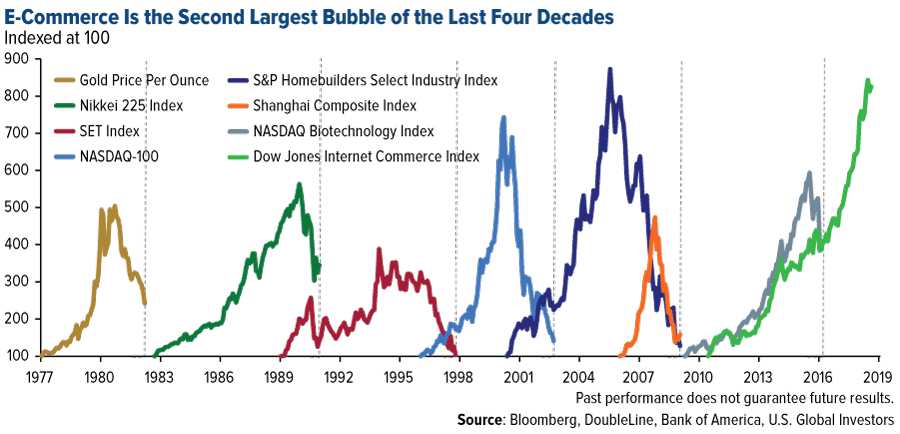

FAANG stocks have soared in recent months like there is no tomorrow. In fact, Amazon, Apple, etc. have shot up nearly eight times since March 2010 according to a recent article by Frank Holmes of U.S. Global Investors. The bubble in the e-commerce sector is the second largest bubble in the past four decades as shown in the chart below:

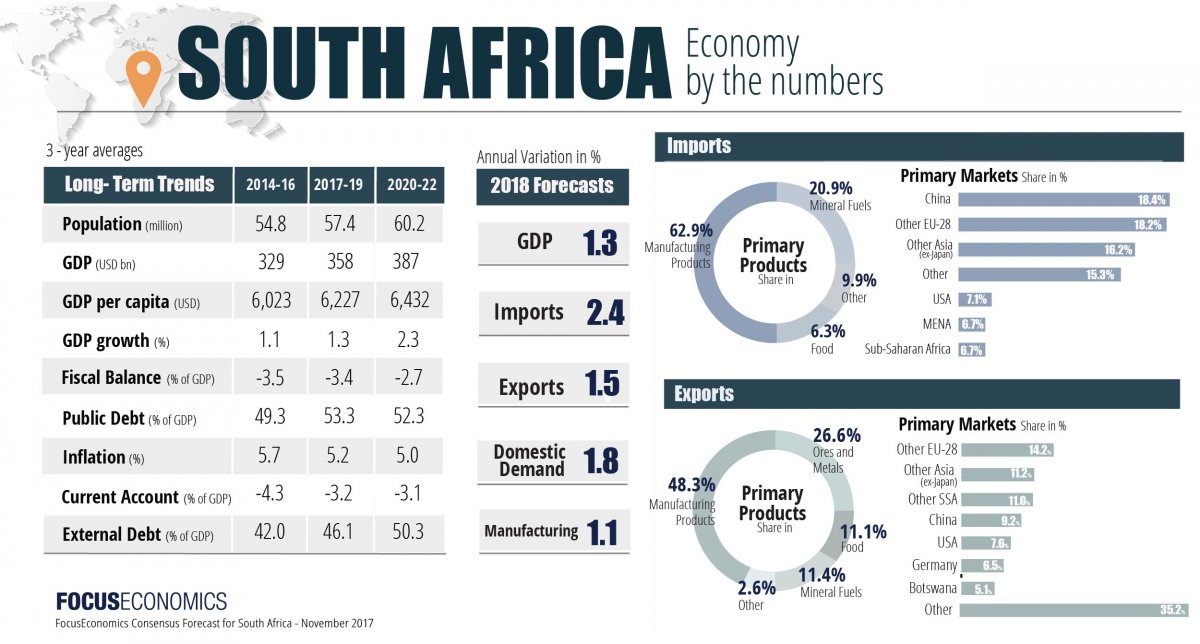

South Africa is one of the major emerging economies. Though the country is rich in natural resources and is considered as a commodity-based economy, exports of manufacturing products accounts for nearly half of the economy and ores and metals constitute only one-fourth of exports.

The following infographic shows a snapshot of the key variables of the South African economy:

Emerging market stocks are riskier than developed world stocks for the obvious reason that those markets are still developing – meaning institutions, rule of laws, regulations, policies, intellectual protection, etc. are still a work in progress. Hence investors investing on stocks from these countries are betting that despite these disadvantages companies would grow their profits and perform better than their developed peers. In addition, the saying goes taking bigger risks leads to bigger returns. This is true in emerging markets. Though emerging market equities can be extremely volatile in the short-term, they outperform developed world stocks in the long run. Investors who are able to wait out the stomach churning plunges in these stocks are rewarded well over the long-term.

For example, the S&P 500 is up by 8.76% YTD based on price alone. Compared to this solid return, some of the emerging markets’ returns are listed below:

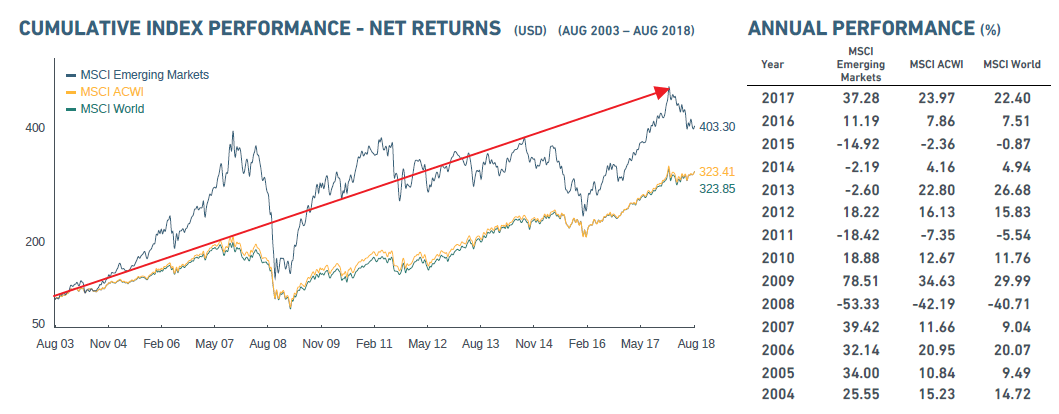

Just because these indices are down relative to the US market YTD does not mean they are poor performers over the 5, 10 or even 20 year time frames. In fact, these equities have beaten or generated comparative returns to the US market over the long run.The following chart shows the performance of the popular benchmark MSCI Emerging Markets Index from Aug 2003 thru Aug 2018:

In a recent post JEFFREY KLEINTOP of Schwab discussed the volatility of emerging markets and the solid returns they deliver over the long term. From the piece:

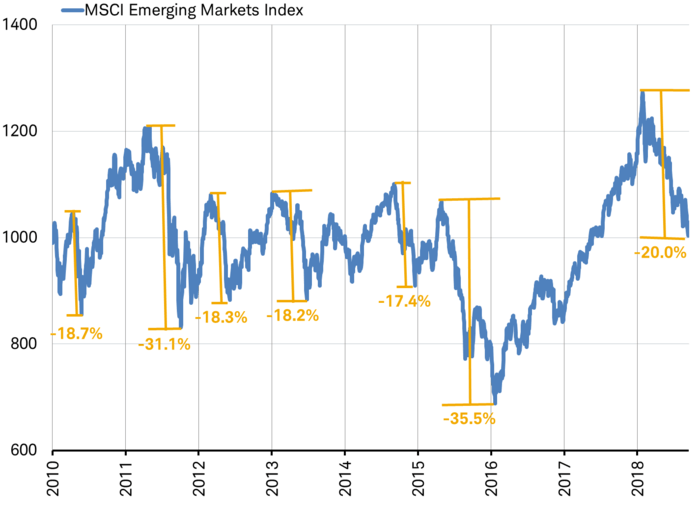

Emerging market stocks are highly volatile in the short-term—about twice as volatile than other equity asset classes. During almost every one of the past nine years the EM index has fallen around -20% or more only to bounce back, as you can see in the chart below.

Frequent pops and drops

Source: Charles Schwab, Bloomberg data as of 9/14/18. Past performance is no guarantee of future performance.

With this kind of annual volatility, timing the tops and the bottoms is nearly impossible given how rapidly and frequently they happen. Looking back since the inception of the EM index we can see in the table below that once it has fallen 20%, it is usually up double-digits just six months later—unless it is the end of the global economic cycle (2000, 2008). The end-of-cycle declines have been longer and deeper.

Rapid rebounds often follow 20% declines

Past performance is no guarantee of future performance.

Source: Charles Schwab, Factset data as of 9/11/18.

Jeff noted that the benchmark index has declined by 20% or more in 7 of the past 9 years but has sharply bounced back.

A few takeaways:

Emerging market stocks are not for the faint-hearted. If an investor cannot tolerate 20 to 50% falls within a short period of time, they should avoid these markets.

With individual stocks, it is highly important to be selective.

For many investors, the easiest option is to go with an ETF than trying to pick winners.

Some of these markets are dominated by just a handful of companies. Hence over-concentration risk has to be taken into consideration.

To protect from any blowups of a particular country or a sector, it is important to diversify across many countries and sectors.