How do the government expenditures of USA and Norway differ?. USA follows the capitalist economic model whereas Norway is a socialist country. It is a general notion that the US spends less on social entitlement programs compared to socialist countries. When we compare the expenditures of Norway and US using the charts below, there is not much difference between these countries especially when it comes to social programs.

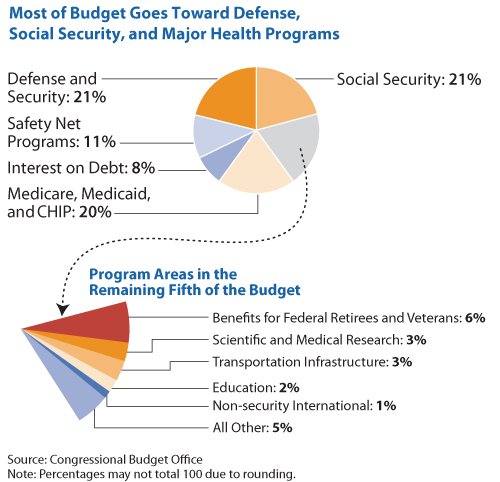

USA – The Federal Budget for 2008

Norway – Government Expenditures in 2008

Source: Statistics Norway

The top 3 areas of US expenditures are : Defense and Security, Social security, Medicare and the like. The US spent 21% of the budget on defense and security compared to under 5% by Norway in 2008. This is understandable since the US maintains hundreds of military facilities worldwide and currently runs two wars.

Norway spent about 55% on social benefits and health-care. The total expenses spent on Social Security, Medicare, Medicaid and CHIP and Safety Net Programs equaled 52%. This comparison clearly shows that the US spends more than half of the budget on social programs. Despite being a capitalist country, it shows that the government has become socialistic over the years. Though the “public” option has been eliminated from the health care reform, Uncle Sam is the main provider of health insurance for most of the senior citizens thru Medicaid and Medicare. All these entitlement programs cost the government a lot of money and will continue to grow in the future. Some say that the government run entitlement programs such as the Social Security is the largest ponzi scheme of all as majority of the funds needed for these programs are borrowed from lenders or paid out of tax revenue from workers.

Since Norway is a surplus country it does not have interest payments. As of July this year the US budget deficit amounted to $1.3 Trillion. This US borrows heavily from other countries including the major lenders China and Japan to fund its operations. As a result , 8% of the US budget goes to the payment of interest on national debt. In 2008, the total interest payments were $253 B. As more funds of borrowed to finance additional social welfare programs and the various corporate bailout programs like TARP, this part of the budget will definitely increase. From another perspective, one can say that 8% of the national expenditure went to waste unnecessarily in the form of interest payments.

The remaining 19% of the US budget went to all other areas such as education, transportation infrastructure,scientific research, etc. It would be better if a higher percentage of government spending is allocated for these areas.