Mr.Jack Bogle, founder of The Vanguard Group is not a fan of foreign stocks. He basically states that Americans need not own foreign stocks since one gain exposure to overseas markets by simply staying with US firms. Jack gave an interview Bloomberg in 2014 and I wrote an article about that.

I admire Mr.Jack for helping millions of investors saving billions with his index investing approach. However I do not agree with his views on international stocks. In a recent interview with MarketWatch he shared the same views he held back in 2014 on foreign stocks. From the interview:

On the index he would pick if he was starting the first index fund again:

Bogle: I would choose the Standard & Poor’s 500 Stock Index SPX, -0.09% for the same reasons I picked it in the first place all those years ago. The reality is that it’s weighted by the market capitalization of each stock, so if a big stock goes up in value, you don’t have to buy any more, it goes up in value by the exact same amount in the fund. It is a very low-transaction costs investment. It’s the best index around.

On people who would criticize that choice because the S&P 500 is a U.S. stock index:

Bogle: I’m out on kind of a limb on this, but I realize — and everyone else should know — that in the S&P 500, almost half of the revenues and half of the earnings of those 500 corporations come from outside the U.S. It is an international portfolio, it just doesn’t have a stock price that floats in the international market.

So I am happy to have a totally U.S. portfolio, and that is what I happen to do myself.

I can’t tell you it’s right. I can’t say that international won’t do better in the future, because it has done so much worse in the past since I first made this statement back in ’93. … You don’t need to use international, however, and if you do, keep it below 20% of your portfolio.

Source: Opinion: Jack Bogle tells you the secret to becoming a winning investor, MarketWatch, Dec 21, 2016

Listed below are five reasons why investors should own foreign stocks. And depending on one’s individual circumstances, allocating more than 20% of one’s portfolio to overseas markets is also smart.

- No one market is the top performer every year consistently. For example, the US may be the top performing market one year but the next year it can end up with average returns.

- Many foreign markets have dividend yields that are much higher than the pathetic 2% yield of the S&P 500. For instance, UK’s FTSE 100 yield is about 4%. Similarly Australia, New Zealand have yields that are far higher than that of US firms.

- The US is a world-class leader in certain sectors but not all sectors. For instance, in technology American firms put the rest of the world’s firms to dust. Though there are a few European tech pioneers, majority of the top tech firms like Amazon(AMZN), Facebook(FB), Netflix(NFLX), Alphabet (GOOG),etc. are US companies. No other country can match the US in the high-tech field. But there are other industries where the US lags other countries. In the chemical industry, Germany firms such as BASF AG(BASFY) top global rankings. Similarly in consumer products European firms like Unilever(UN) and Nestle(NSRGY) beat their US rivals. So in order to profit from the world leaders in sectors, investors should cast their net far and wide.

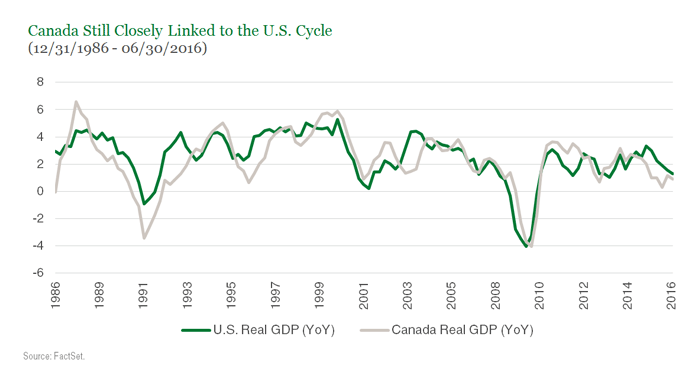

- In banking, the US is not the best always. The recent Global Financial Crisis(GFC) proved that the seemingly stable US banks were nothing more sand castles. Compared to many US banks, the banking industry in countries like Canada and Australia are far superior and banks in those countries were mostly unscathed during the awful crisis of 2008-09. So an investor that was stuck with purely US bank stocks would have lost or under-performed than an investor owing Canadian and Aussie banks.

- Though Mr.Jack points out that more 50% of revenues of S&P 500 firms come from abroad and that gives international exposure to US investors, simply owning S&P 500 firms is not a great way to access foreign markets. While there are many reasons for this, one reason is that American firms may earn a lot from foreign markets but that does not necessarily they will share the gains with investors. For instance, large-cap US firms are known for their obsession with stock buybacks to boost share prices and acquisitions. Many studies have proven that buybacks do not benefit ordinary shareholders as much as say higher dividend payouts. By investing directly in foreign companies, an investor avoids the wasteful and outlandish behavior of large US corporations with their profits.

Related ETFs:

- iShares MSCI Canada Index (EWC)

- iShares MSCI Australia Index (EWA)

- Global-X Norway ETF (NORW)

- iShares MSCI United Kingdom Index (EWU)

Disclosure: No Positions