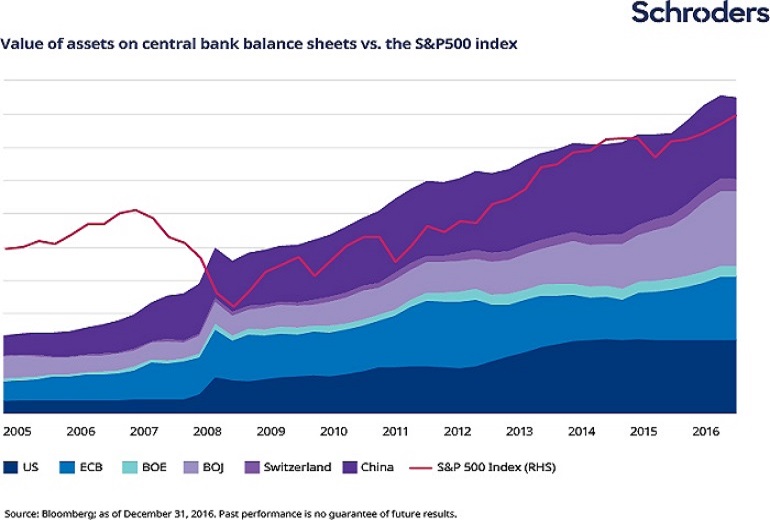

Quantitative easing and negative interest rate policies followed by major central banks in the past few years have been a disaster for savers. However these policies have been a boon to equity investors as asset prices have soared. The following chart shows the relationship between the value of assets on central bank balance sheets vs. the S&P 500 index:

Click to enlarge

Source: Investors should prepare for liquidity inflection point, Schroders