The Price/Earnings ratio (P/E) is sometimes used by investors to identify if equities are cheap or expensive and if getting in when the ratio is lower means higher returns in the future. However an article by Lord Abbett notes that P/E ratio alone is not a good indicator of future market returns.

From the article:

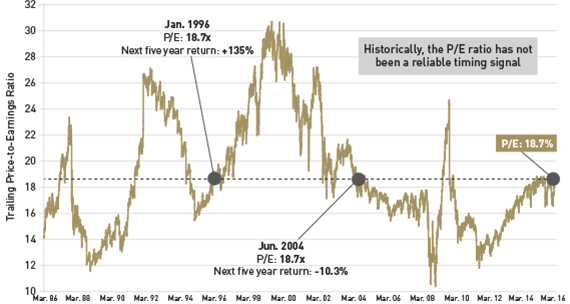

History shows, however, that, in the short run, the P/E ratio has not been a reliable predictor of future market returns. In the past 20 years, for example, the S&P 500 has traded at its current level of approximately 18.7 times trailing earnings twice—once in January 1996 and again in June 2004. What happened over the next five years in each case? The results were very different. Cumulative returns five years out from 1996 reached triple digits; after 2004, returns were negative (see Chart 1).

If P/Es haven’t been reliable predictors of short-term market returns, what about other commonly cited metrics? We’ve looked at a number of them—including the Shiller CAPE ratio, EPS growth, earnings growth, dividend yield, the U.S. Federal Reserve (Fed) model, and U.S. gross domestic product—to assess how well they predict the next 12 months of stock returns. The answer: Not well at all.

Moreover, over the long term, market timing takes a toll on equity fund returns. As a previous blog reported, a Morningstar study in 2014 depicted significant shortfalls over a 10-year period across seven major fund categories caused by poor market timing.

If popular metrics tell us very little about the near-term direction of the stock market, then that should speak to the difficulty of market timing.

Source: Stocks: Put Time on Your Side, Lord Abbett

So the key takeaway for investors is that the P/E ratio alone should not be the deciding factor when making investment decisions. Rather the ratio must be used together with other factors and invest for the long-term.